Most traders understand the idea of buying low and selling high, but they struggle to apply it in real time. When the market is moving quickly, the emotional pull is usually strongest after the easy part of the move has already happened. A trader sees momentum, feels urgency, and starts thinking the move may continue without them.

That is where many poor decisions begin. The trader is no longer evaluating structure, location, or risk. They are reacting to speed.

Extreme to Mean is built around a different idea. Instead of chasing movement, the trader waits for price to reach a meaningful location, studies the context around that location, and then decides whether the setup has earned attention. The goal is not to guess the top or bottom. The goal is to avoid treating every move as an opportunity.

The Market Does Not Move in a Straight Line

Markets expand and contract. They push away from balance, pause, rotate, reset, and sometimes continue. Even strong trending markets do not usually travel in clean straight lines forever. There are stretches, pauses, pullbacks, failed rotations, and continuation attempts.

The "mean" is simply a reference point for balance. Depending on the trader's system, that mean may be a moving average, VWAP, a midline, a prior value area, or another fair-value reference. The exact tool matters less than the concept: price can move away from balance, and the trader can evaluate how stretched that move has become.

An "extreme" is not automatically a trade. This is important. Price can stay extended longer than a trader expects, especially during news, trend days, high-volume breakouts, or emotional market conditions. The edge is not in blindly fading every stretch. The edge is in recognizing when price is stretched, then waiting for evidence that the move is losing control or rotating back toward balance.

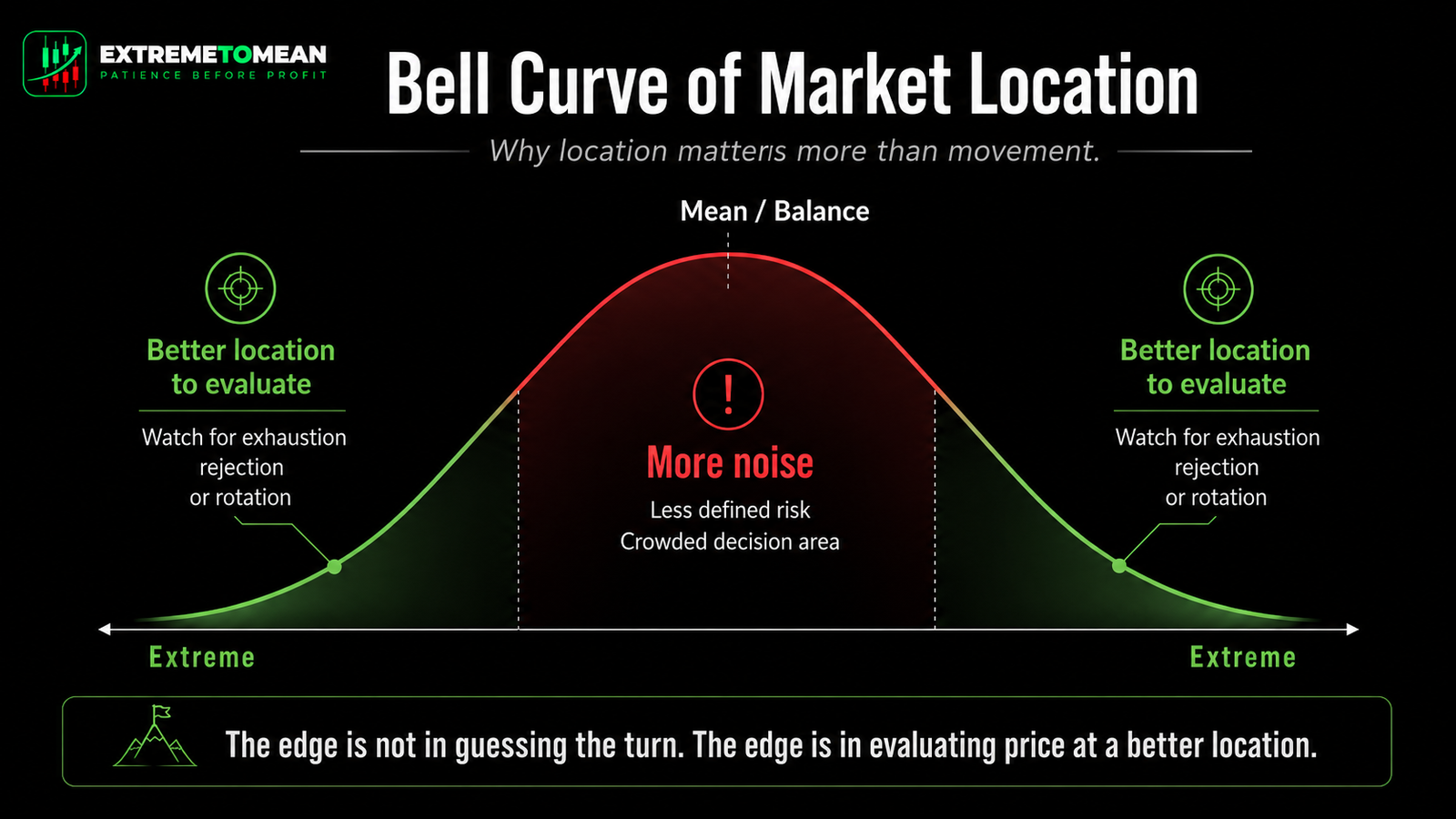

The Bell Curve Behind the Concept

A simple way to understand Extreme to Mean is through the bell curve. In many market conditions, a large amount of normal price activity happens around a central area of value. Price may move above or below that area, but the farther it stretches, the less "normal" that location becomes relative to the recent auction.

That does not mean price must snap back immediately. It only means the trader should become more aware of context. At the middle of the curve, price is often less attractive because risk can be less defined and direction can be less clear. Near the edges, the trader may have a cleaner location to evaluate.

This is why location matters. The middle often creates confusion because both sides can still make a reasonable argument. Buyers may see a pullback. Sellers may see resistance. Price can chop, fake out, and trap both sides.

At an extreme, the question becomes more focused: has price stretched far enough that the next clean decision may come from exhaustion, rejection, or rotation? That question does not guarantee a trade. It simply gives the trader a more disciplined place to begin evaluating.

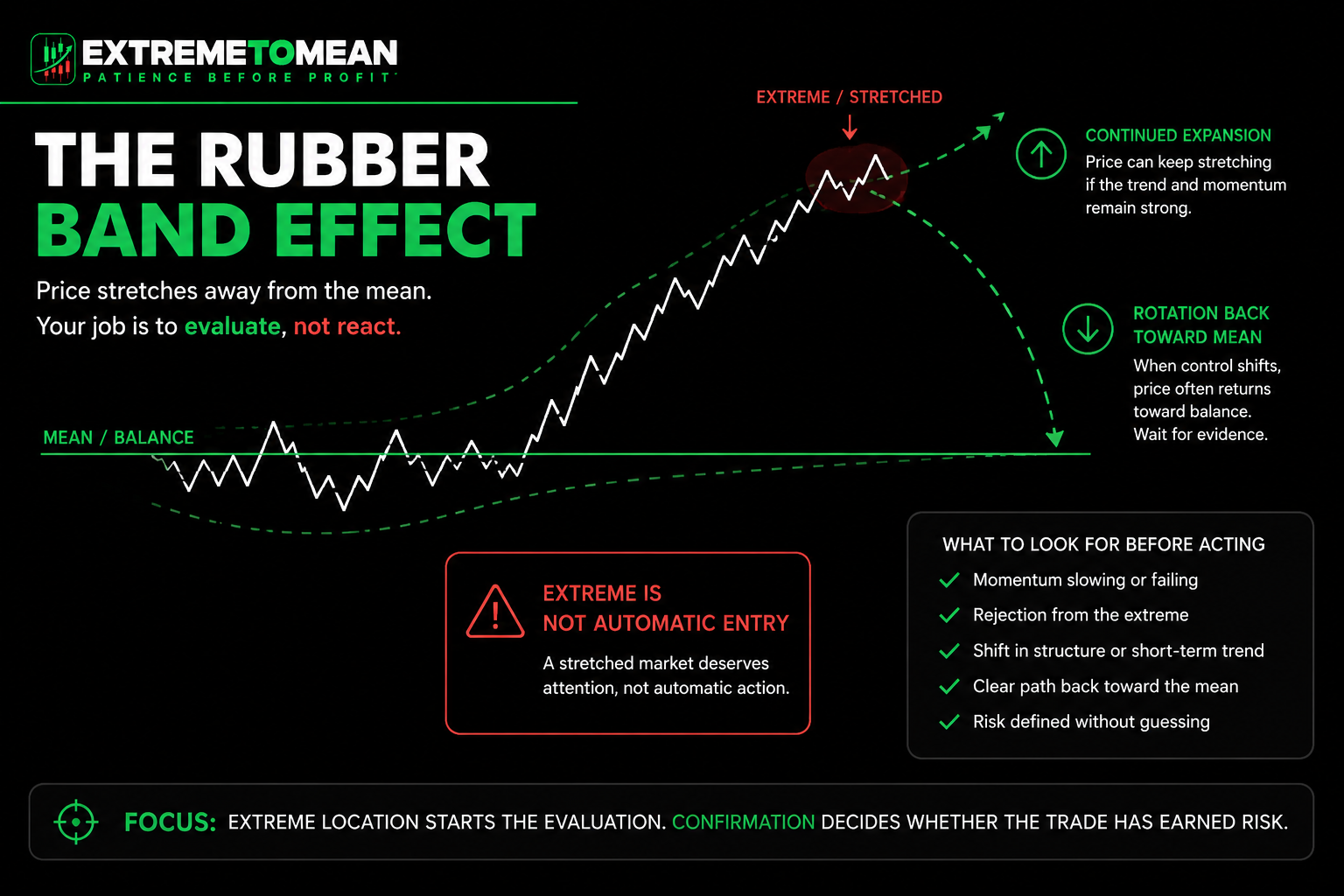

The Rubber Band Effect

The rubber band effect is another useful way to think about Extreme to Mean. When price stretches away from a reference point, it can begin to act like a rubber band under tension. The farther it stretches, the more attention the trader should pay to whether the move is still being supported.

But a stretched rubber band can do two things. It can snap back, or it can keep stretching until the structure changes completely. That is why patience is essential. A trader who enters just because price is extended may be early, and being early can feel the same as being wrong when risk is not clearly defined.

This is where many traders get trapped. They see the market at an extreme and assume the reversal should happen now. Then price pushes one more level, stops them out, and finally rotates after they are gone. The idea was not necessarily wrong, but the timing, confirmation, or risk plan was not clean enough.

Extreme to Mean thinking does not ask, "Is this too high?" or "Is this too low?" Those questions are usually incomplete. A better question is: "Is price extended, and is there evidence that control is shifting?"

Why the Mistake Feels Reasonable

Chasing the middle feels reasonable because the market often looks most obvious after it has already moved. A strong green candle feels bullish. A sharp red candle feels bearish. A breakout feels like confirmation. A fast selloff feels like danger.

The problem is that obvious movement is not always clean opportunity. By the time the trader feels certain, price may already be far from a good entry location. Risk may be harder to define. The stop may need to be wider. The target may be closer than it appears. The trader may be entering where better traders are reducing risk, taking profits, or waiting for the next rotation.

This is one of the hardest lessons in trading: the best-looking move is not always the best decision. Sometimes the cleanest trade comes after waiting for price to reach a better location. Sometimes the best trade is no trade at all.

Patience Before Profit means the trader does not force a decision just because the chart is moving. The setup has to earn attention. Then it has to earn risk.

What a Better Trader Looks For

A better trader does not treat every extreme as an automatic reversal. They evaluate the condition of the move. They ask whether price is stretched into a meaningful area, whether momentum is changing, whether structure is supporting the idea, and whether risk can be defined without forcing the trade.

This process creates a cleaner decision. The trader is no longer reacting to fear of missing out. They are studying location, context, and behavior around the extreme.

A cleaner Extreme to Mean decision may include signs such as slowing momentum, failed continuation, rejection from an outer band, a shift back through a short-term average, or a rotation toward a known mean. None of these signs guarantees the outcome. They simply help the trader decide whether the setup is organized enough to consider.

The key difference is that the trader is evaluating instead of predicting. Prediction says, "This has to reverse." Evaluation says, "Price is extended, but I need evidence before I act."

A Practical Extreme-to-Mean Decision Filter

Before taking a trade based on an extreme, a trader can slow the decision down with a simple filter:

- Is price actually stretched from a meaningful reference point?

- Is this an extreme within normal conditions, or is the market in a strong trend or news-driven expansion?

- Is there evidence that momentum is slowing or control is shifting?

- Is the potential mean or target area clear?

- Can risk be defined without guessing?

- Am I entering because the setup is clean, or because I feel late?

The better question is not, "Will this reverse?"

The better question is, "Has this extreme created a clean enough decision for me to define risk and evaluate a rotation back toward the mean?"

That question changes the trader's job. The trader is no longer trying to be early, clever, or right. The trader is waiting for conditions that make the decision cleaner.

Final Thought

Extreme to Mean is really about patience at the edge of imbalance. It teaches the trader to stop chasing the middle, respect location, and wait for better evidence before committing risk.

The market will never be fully predictable. Price can stretch farther, reverse sooner, or stay messy longer than expected. The trader's job is not to know what comes next. The trader's job is to evaluate whether the current location, context, and structure are clean enough to make a disciplined decision.

Patience comes first. The setup has to earn attention before it earns risk.

Educational content only. Trading involves substantial risk and is not suitable for everyone.