New traders often look at “the market” as if it is one thing. They see the S&P 500 up, a tech stock down, Nasdaq futures moving, or an ETF holding above support, and they treat each one as if it is giving the same message. That is where confusion starts.

The market is not one single object. It is a collection of benchmarks, groups, individual companies, contracts, and tradable products. Each one can be useful, but each one answers a different question. A trader who does not understand that difference can end up reacting to the wrong signal.

This is why basic market structure matters. Before a trader studies entries, candlesticks, or signals, they need to understand what they are reading and what that information is actually telling them. That is one of the core ideas behind the broader market context lessons inside Extreme to Mean.

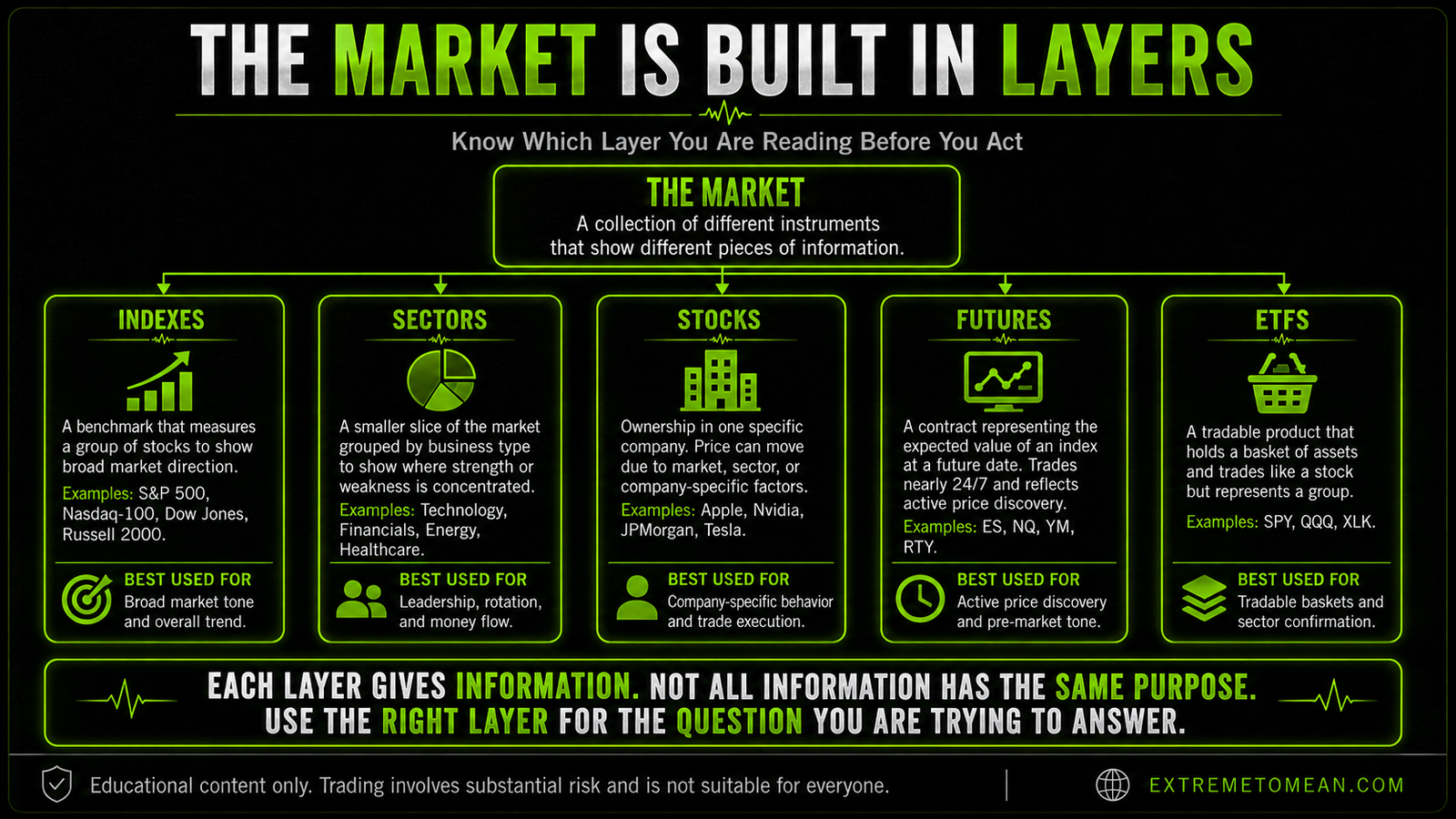

The Market Is Built in Layers

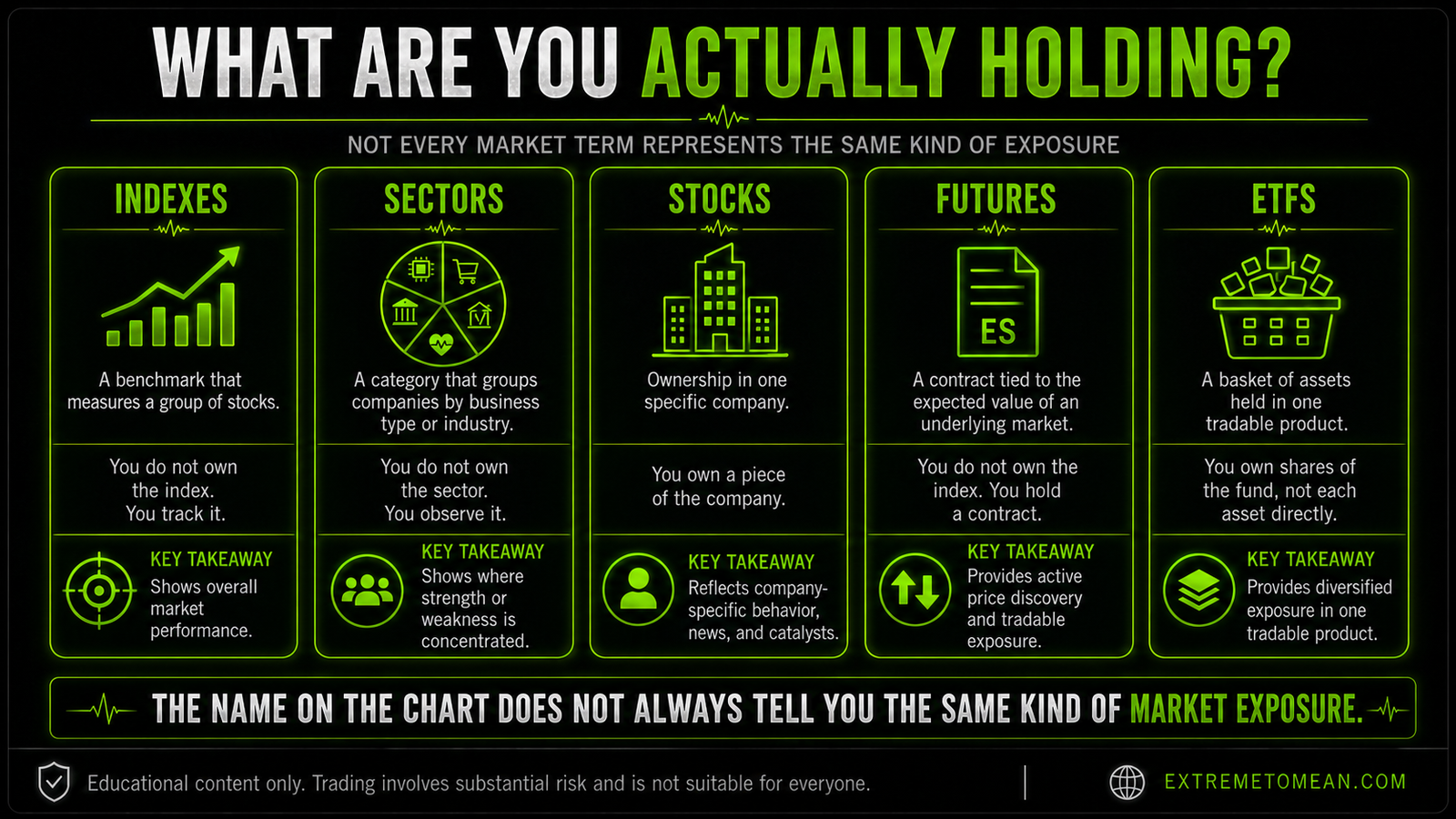

When people say “the market is up,” they are usually talking about an index. An index is a benchmark. It measures a group of stocks and gives traders a quick way to understand broad market direction. The S&P 500, Nasdaq-100, Dow Jones Industrial Average, and Russell 2000 are common examples.

A sector is a smaller slice of the market. Instead of measuring many different types of companies together, sectors group companies by business type. Technology, financials, energy, healthcare, consumer discretionary, and industrials are examples of sectors. Sectors help traders see where strength or weakness is concentrated.

A stock is ownership in one specific company. Apple, Microsoft, Nvidia, JPMorgan, Tesla, and Exxon are individual stocks. A stock can move because of the broad market, its sector, company-specific news, earnings, analyst comments, or investor positioning.

A futures contract is different. Futures are contracts that trade based on the expected value of an underlying market at a future point in time. ES futures track the S&P 500, NQ futures track the Nasdaq-100, YM futures track the Dow, and RTY futures track the Russell 2000. Futures often trade nearly around the clock, which means they can move before the regular stock market opens.

An ETF, or exchange-traded fund, is a tradable product that usually holds a basket of assets. SPY tracks the S&P 500, QQQ tracks the Nasdaq-100, IWM tracks the Russell 2000, and sector ETFs like XLK, XLF, and XLE track specific sectors. ETFs trade like stocks, but they often represent a group of holdings instead of one company.

Each layer gives information, but not all information has the same purpose. An index helps define broad tone. A sector helps identify where money is flowing. A stock shows company-specific behavior. A futures contract shows active price discovery, especially outside regular hours. An ETF gives traders a liquid way to trade or track a basket.

A better trader does not ask, “Is the market up or down?” and stop there. A better trader asks, “Which layer of the market is moving, and does that layer actually matter for the trade I am considering?”

Why Confusion Creates Bad Reads

The mistake usually feels reasonable in the moment because the charts look connected. If Nasdaq futures are pushing higher, it can feel natural to assume every technology stock should be strong. If the S&P 500 is green, it can feel like the whole market is healthy. If one large stock is ripping higher, it can feel like the broader index must be strong too.

That is not always true.

An index can rise because a small group of heavy-weighted stocks are carrying it. A sector can be strong while the broader market is mixed. A stock can break down even while its sector holds up. Futures can move overnight because of global markets, economic data, or positioning before cash equities open. ETFs can reflect basket demand, hedging, liquidity, or broad exposure rather than one clean directional message.

This is why “the market is moving” is not enough. A trader needs to know what is driving the move and whether that driver supports the trade idea. The idea that the market comes first does not mean every chart must agree. It means the trader should understand the environment before treating a setup as meaningful.

Confusion becomes dangerous when a trader uses one layer to justify a trade in another layer without checking the relationship. For example, a trader might see ES futures pushing higher and then chase a weak individual stock long just because “the market is green.” That is not context. That is borrowing confidence from the wrong chart.

The same thing can happen in reverse. A trader might see one major stock selling off and assume the whole market is breaking, even though the broader index remains controlled and other sectors are rotating higher. Without context, the trader reacts to noise and mistakes it for information.

The Risk Is Treating Proxies Like Proof

A proxy is something traders use to represent something else. SPY can be used as a proxy for the S&P 500. QQQ can be used as a proxy for the Nasdaq-100. ES and NQ futures can be used as active proxies for broad market tone. Sector ETFs can be used as proxies for sector strength or weakness.

Proxies are useful, but they are not proof.

This matters because traders often build a trade idea from partial information. They see futures green, a sector ETF holding support, or a major stock moving, and they treat that as enough. But a proxy only gives a clue. It does not replace structure, location, risk, or confirmation on the instrument being traded.

For Extreme to Mean traders, this is especially important because reversion-based decisions depend on context and location. If price is stretched, the trader still needs to know what kind of stretch it is. Is the move broad market strength? Is it sector rotation? Is it one stock-specific event? Is it an overnight futures move that may change after the open? Is it an ETF move caused by basket demand?

A setup can look cleaner when the trader understands the source of the move. A setup can also become weaker when the context does not support it. That is why market conditions can change the quality of a setup, even when the pattern itself appears familiar.

The risk is not that proxies are bad. The risk is using them lazily. A trader who says, “QQQ is up, so this trade is good,” has not done enough work. A trader who says, “QQQ is up, XLK is leading, NQ is holding above prior resistance, and the stock I am watching is pulling back into a clean location,” is working with a more complete read.

The difference is process.

What Each Market Layer Is Best Used For

A cleaner approach is to assign a job to each layer of the market. Instead of treating every chart as the same kind of signal, use each one for the information it is best suited to provide.

Indexes are best used for broad market tone. They help answer whether the major market averages are risk-on, risk-off, mixed, or rotational. They are useful for understanding the background environment, but they are not always enough to define the quality of an individual trade.

Sectors are best used for leadership and rotation. If the broad market is green but only defensive sectors are leading, that tells a different story than technology, consumer discretionary, and small caps all pushing higher together. Sector behavior helps traders understand whether strength is broad or narrow.

Stocks are best used for specific execution decisions. A stock has its own structure, volume, volatility, catalysts, and levels. Even when the market context is supportive, the actual trade still has to make sense on the instrument being traded.

Futures are best used for active price discovery and intraday tone. They are especially helpful before the regular session opens because they show how traders are pricing the index outside normal stock market hours. Futures can give useful context, but they can also move quickly around data, news, and liquidity shifts.

ETFs are best used for tradable baskets and confirmation. They can help a trader see whether a group is participating. They can also provide cleaner views of sector or index behavior without focusing on one individual stock.

This does not mean a trader needs to watch everything. Watching too many charts can create its own problems. The point is to know why each chart is on the screen. If a chart does not answer a useful question, it may be adding noise instead of clarity.

This connects directly to location. A trader may identify a strong market backdrop, but if the actual instrument is sitting in the middle of a messy range, the trade may still be poor. Context helps, but location still matters. That is why location is the first filter before risk deserves attention.

A Practical Filter Before You Act

Before acting on a market move, slow the decision down. The goal is not to predict every layer perfectly. The goal is to avoid reacting to one piece of information as if it tells the whole story.

Use this simple filter:

- What am I actually trading?

- What market layer am I using for context?

- Is that layer directly related to the trade?

- Is the move broad, sector-specific, stock-specific, or futures-driven?

- Does the instrument I want to trade agree with the context?

- Is price at a location where the setup earns attention?

- Is the risk clear before the entry?

The better question is not, “Is the market moving?” The better question is, “Is the part of the market I am reading actually relevant to the risk I am about to take?”

That question can keep a trader from forcing weak connections. It can stop a trader from chasing a stock just because futures are green. It can stop a trader from shorting an index because one large company is weak. It can also help a trader recognize when conditions are mixed and the better decision is to wait.

Waiting is not passive. Waiting is part of evaluation. If the layers do not line up clearly enough, the trader does not need to invent confidence. The setup has not earned risk yet.

For traders building a process from the ground up, it helps to begin with a structured path instead of trying to interpret every chart at once. The beginner trading path is designed to help traders slow down, organize the market, and build better decision habits before focusing on execution.

Final Thought

Indexes, sectors, stocks, futures, and ETFs are connected, but they are not interchangeable. Each one gives a different view of market behavior, and each one can be useful when the trader understands its role.

The mistake is treating every movement as the same message. The better process is to identify the layer, understand what it is telling you, and decide whether that information actually supports the trade in front of you.

A trader’s job is not to react to every green or red chart. A trader’s job is to evaluate context, location, and risk before acting.

Educational content only. Trading involves substantial risk and is not suitable for everyone.