Futures can confuse beginners because they often look simple on a trading platform. You may see symbols like ES, NQ, YM, RTY, CL, GC, or BTC futures. You may see a chart moving up and down. You may see candles, volume, price levels, and a buy or sell button.

But behind that chart is a contract.

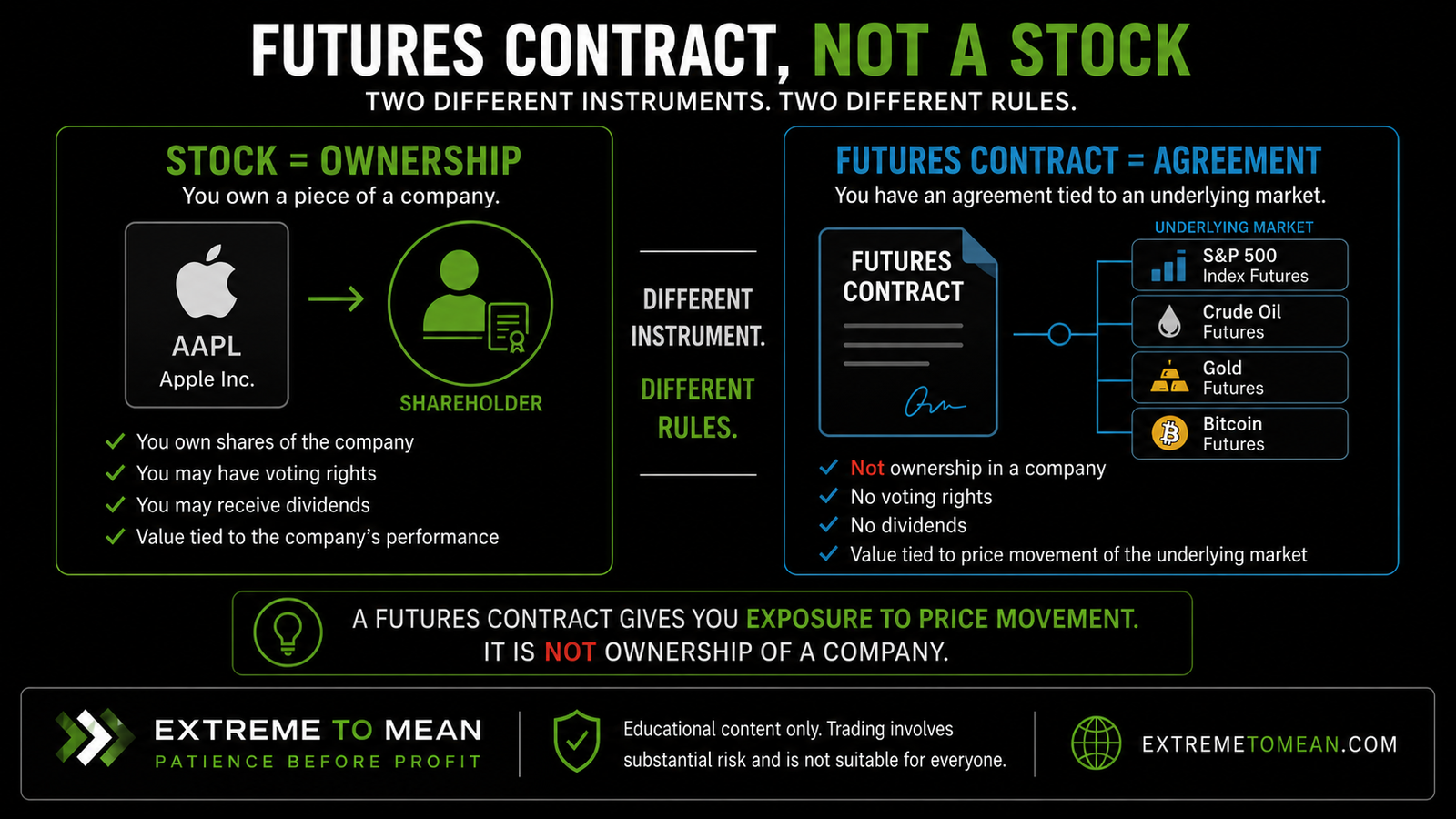

That matters because futures are not ownership in a company. They are not ETFs. They are not mutual funds. They are standardized agreements tied to an underlying market, such as a stock index, commodity, currency, interest rate, or cryptocurrency-related benchmark.

At Extreme to Mean, futures matter because many active-trading lessons reference contracts, ticks, intraday movement, margin, and risk. Before a trader can evaluate a setup, they need to understand what instrument they are actually trading. This is why futures belong inside the broader Basics trading education path, even before deeper lessons on entries, setups, and execution.

A Futures Contract Is an Agreement, Not Ownership

When you buy a stock, you are buying ownership interest in a specific company. If you buy shares of Apple, you own shares tied to Apple as a business. The stock price reflects what buyers and sellers are willing to pay for that ownership interest.

A futures contract works differently.

A futures contract is an agreement between buyers and sellers based on the future price of an underlying asset or market. That underlying market could be crude oil, gold, the S&P 500, the Nasdaq-100, the Dow, Treasury bonds, agricultural products, currencies, or other markets.

For example, an index futures contract does not give you ownership of the index. It gives you exposure to price movement tied to that index. If the contract moves in your favor, your account reflects that gain. If it moves against you, your account reflects that loss.

This is a different concept from what a stock really is. A stock is tied to ownership of one company. A futures contract is tied to an agreement based on an underlying market.

That distinction matters because the risk is different. A beginner who treats a futures contract like a cheap version of a stock can misunderstand how quickly gains and losses can change. The chart may look familiar, but the mechanics underneath are not the same.

Why Futures Exist

Futures were not created only for day traders. They exist because businesses, institutions, investors, and traders need ways to manage exposure to future price changes.

A farmer may want to lock in a future selling price for a crop. An airline may want to manage fuel price exposure. A portfolio manager may want to hedge stock market risk. A trader may want to participate in price movement without buying the underlying asset directly.

In simple terms, futures help market participants transfer and manage price risk.

That does not mean every futures trader is hedging a business need. Many active traders use futures because they are liquid, standardized, and available across major markets. But the product still comes from the same basic idea: a contract tied to future price movement.

This is why futures connect naturally to market context. A trader watching S&P 500 futures is not watching one company. They are watching a contract tied to broad index exposure. If you have already learned what an index is, futures are one step further: the index is the measurement, while the futures contract is one tradable instrument tied to that measurement.

The cleaner your language, the cleaner your thinking becomes. You are not “buying the market” in a vague way. You are trading a specific contract with specific rules.

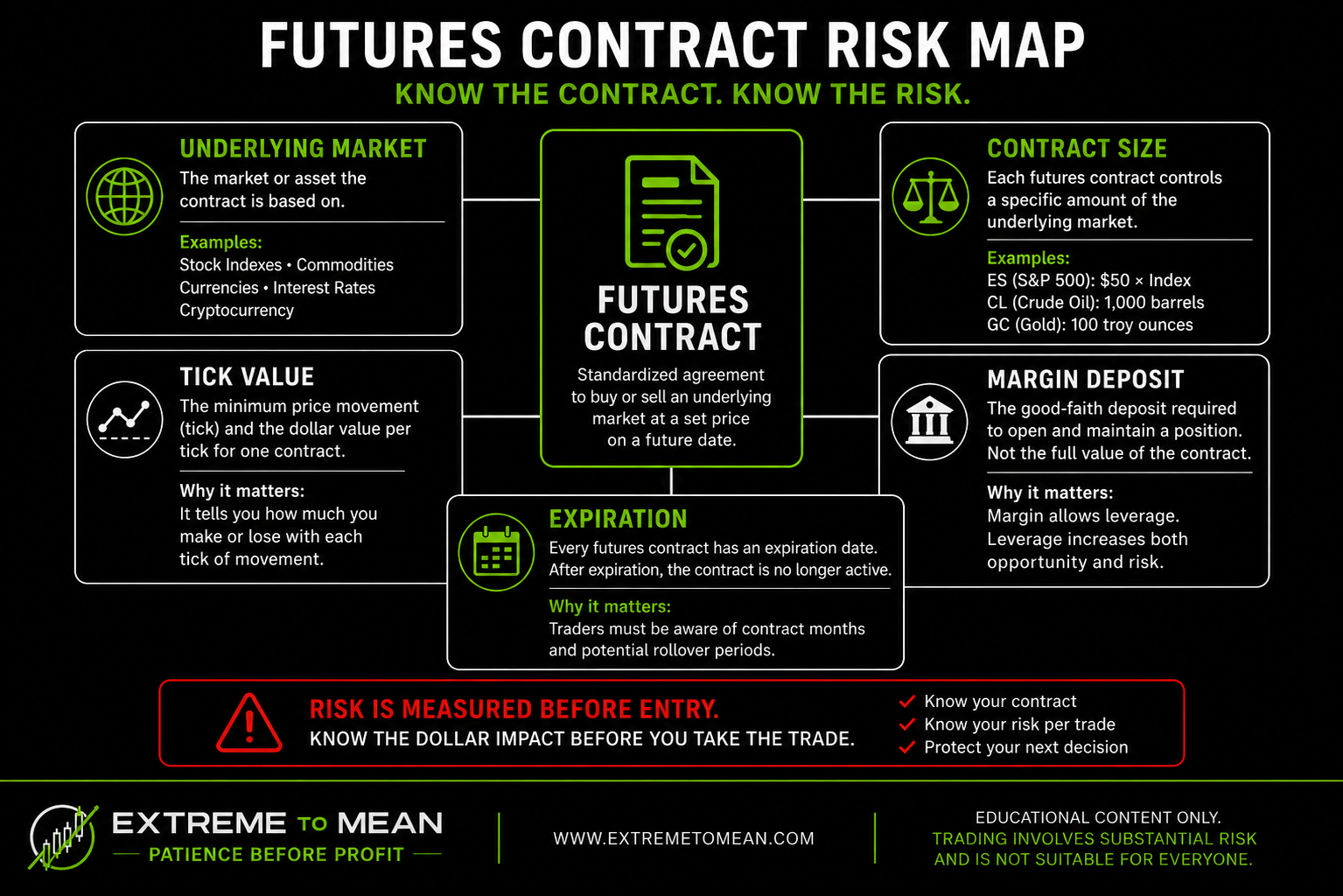

Contract Size, Tick Value, and Why Small Moves Matter

One of the most important futures concepts is contract size.

A futures contract controls a standardized amount of exposure. That exposure is not always obvious from the chart. Two futures products can both move one point on the screen, but that one-point move may not have the same dollar value.

This is where tick size and tick value matter.

A tick is the minimum price movement of a futures contract. Tick value is the dollar value of that minimum movement. If a contract moves one tick, the profit or loss changes by that tick value per contract.

For example, one futures contract may move in small increments worth a few dollars per tick. Another may have a different tick size and a different tick value. Some contracts are larger. Some have micro versions designed to represent smaller exposure. The symbol matters, because the contract specifications matter.

This is where beginners can get into trouble. They may look at a chart and think, “It only moved a little.” But in futures, a “little” movement can mean different things depending on the contract and position size.

The better question is not, “How far did the chart move?”

The better question is, “How much does each tick or point mean in dollars for this contract and for my position size?”

That question turns a visual chart into a risk calculation. It also makes clear why futures cannot be treated casually. Every trade has a mechanical dollar impact, and the trader needs to know that before acting.

Margin Is Not the Same as Buying the Whole Contract

Another beginner confusion is margin.

In futures, margin is not the full purchase price of the contract. It is usually a good-faith deposit required to open and maintain the position. The contract gives exposure to a larger notional value, while the margin requirement is the amount required by the broker or exchange to hold the trade.

This is where leverage enters the picture.

Leverage means a trader can control exposure larger than the cash required to enter the position. That can make futures efficient, but it also makes them dangerous when misunderstood. A smaller required deposit does not mean the risk is small.

The market does not care how little margin was required to enter. The account still responds to the full movement of the contract. If price moves against the position, losses can build quickly relative to the amount posted as margin.

This is one reason Extreme to Mean emphasizes risk before action. A trade should not earn attention simply because the setup looks interesting. It needs clear invalidation, realistic position size, and an understanding of what each tick or point means.

Margin helps explain why futures are active trading instruments, but it does not remove the need for discipline. It increases the importance of discipline.

Futures Have Expiration

Futures contracts also have expiration dates. This is another major difference from stocks.

A stock can continue trading as long as the company remains listed. An ETF can continue trading as long as the fund remains active. A futures contract is tied to a specific contract month or expiration cycle. Eventually, that contract expires.

Active futures traders need to know which contract they are trading. They also need to understand rollover, which is the process of moving attention from an expiring contract to a later contract month. Around rollover periods, volume may shift from one contract to another.

Beginners may not notice this at first. They may simply type in a symbol, open a chart, and assume all price action is the same. But futures symbols, contract months, and expiration matter.

If a trader is watching the wrong contract or trading a contract with thinning liquidity, the chart may not reflect the cleanest active market. Liquidity means how easily a market can be bought or sold without excessive friction. For active traders, liquidity matters because it affects execution, spreads, and trade management.

This is not meant to make futures sound mysterious. It is meant to make the instrument real. Futures have rules. Those rules need to be understood before the trader starts focusing on setups.

Futures Are Built for Active Trading, But They Still Require Process

Futures can appeal to active traders because they offer direct market exposure, liquidity in major contracts, clear contract specifications, and movement during extended trading hours. They are commonly used by traders who focus on indexes, commodities, bonds, currencies, or other broad markets.

But none of that makes futures easy.

A moving futures contract can create urgency. Price may shift quickly. A trader may feel pressure to enter because the chart appears to be leaving without them. The speed of the instrument can make emotional decisions feel reasonable in the moment.

That is exactly where process matters.

At Extreme to Mean, the contract is not the edge. The chart is not the edge. The setup must still earn attention, and the risk must still be clear before the trade earns capital. Futures simply make that discipline more important because the product is leveraged and mechanically precise.

This is why futures connect directly to setup and risk lessons. Before a trader thinks about entry, they need to know the contract, tick value, margin impact, expiration, and the risk level that invalidates the trade idea.

A futures contract can be a useful active-trading instrument. It can also punish confusion quickly. The difference is not confidence. The difference is process.

A Simple Futures Decision Filter

Before trading a futures contract, a beginner should slow down and identify the instrument clearly. The goal is not to predict what the market will do next. The goal is to know what product is being traded and what risk is attached to the decision.

A simple futures filter can help:

- What futures contract am I looking at?

- What underlying market does it track?

- What is the contract size?

- What is the tick size and tick value?

- Is there a micro version or smaller contract available?

- What is the current active contract month?

- When does the contract expire?

- What margin is required, and what exposure does that margin control?

- What is the dollar risk if price reaches my invalidation level?

- Am I evaluating a setup, or reacting to movement?

The better question is not, “Do I think this futures contract will go up or down?”

The better question is, “Do I understand the contract well enough to define the risk before I take the trade?”

That question fits the Extreme to Mean process. Context comes first. Setup comes second. Risk decides whether the trade deserves capital.

For beginners still building the foundation, futures should not be approached as just another chart. They should be approached as contracts with rules, costs, leverage, and expiration. If you are still organizing the full product map, you can start with the beginner trading path before moving deeper into real-time trade decisions.

Final Thought

A futures contract is an agreement, not ownership. It gives exposure to an underlying market through a standardized contract with contract size, tick value, margin requirements, and expiration.

That structure is why futures are common in active trading, and also why they demand respect.

The trader’s job is not to react because a futures chart is moving. The trader’s job is to understand the contract, measure the risk, evaluate the setup, and make decisions only when the product and the process are clear.

Educational content only. Trading involves substantial risk and is not suitable for everyone.