Mutual funds are one of the most common investment products in the financial world, but they are not usually the center of active trading education. That can confuse beginners. They may hear about stocks, ETFs, indexes, futures, and mutual funds all in the same conversation and assume they are just different names for similar things.

They are not.

A mutual fund can hold stocks, bonds, cash, or other assets, but the way it is bought, sold, priced, and used is different from a stock or ETF. That structure matters because the tool should match the decision. A long-term investment vehicle and an active trading vehicle are not built around the same timing needs.

This lesson is not about judging mutual funds as good or bad. It is about understanding what they are, how they work, and why active traders usually focus on other instruments. For beginners building their foundation, this belongs inside the broader Basics trading education path.

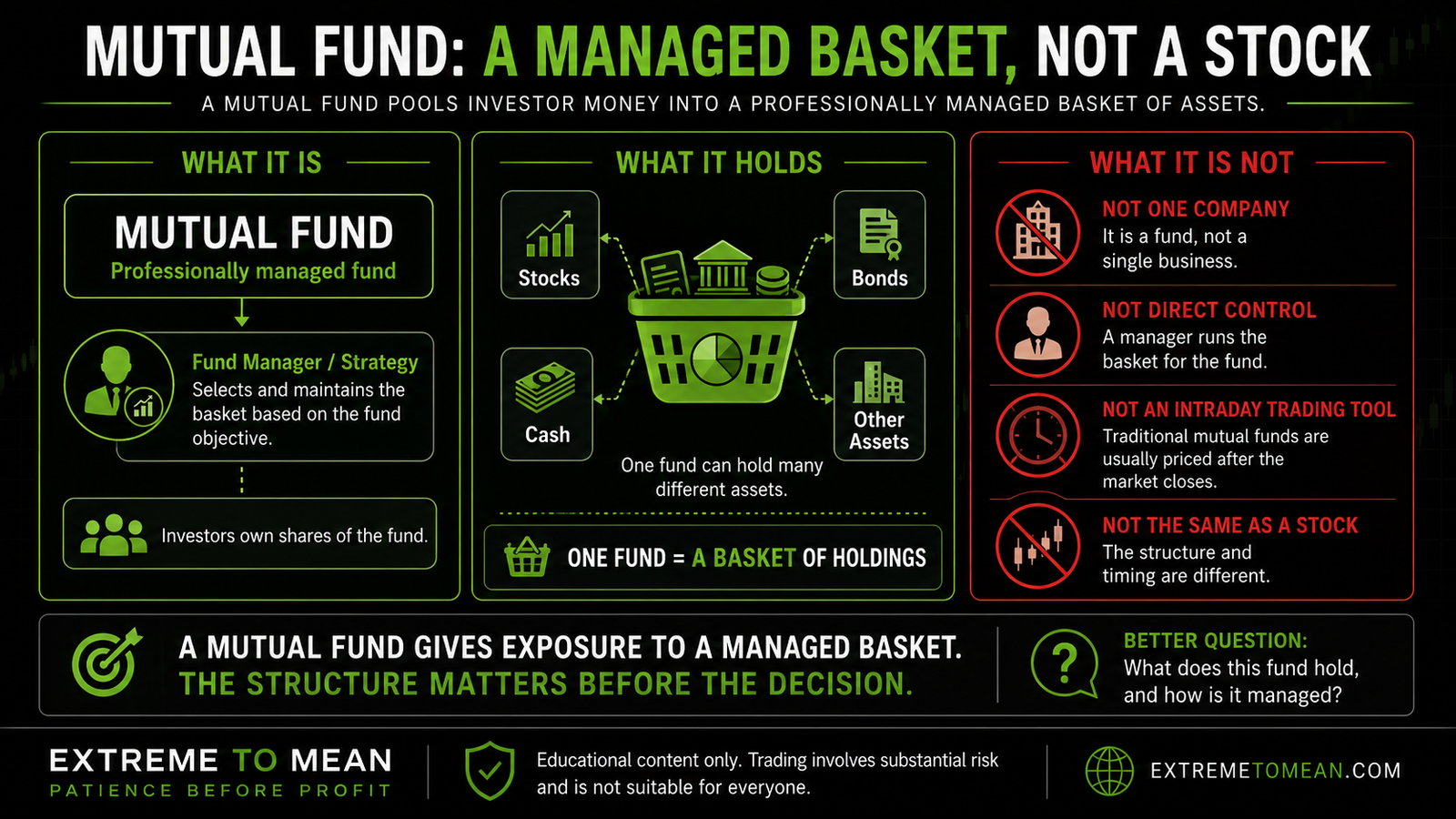

A Mutual Fund Is a Managed Basket

A mutual fund is a pooled investment fund. Many investors put money into the fund, and the fund uses that money to buy a basket of assets. Those assets may include stocks, bonds, money market instruments, or a mix depending on the fund’s objective.

The fund is usually managed according to a stated strategy. Some mutual funds are actively managed, meaning a portfolio manager or team makes decisions about what to buy and sell. Others are index mutual funds, meaning they are designed to track a specific index or benchmark.

The important beginner idea is simple: a mutual fund is not one company.

If you buy a share of a company’s stock, you are buying ownership interest in that specific business. If you buy shares of a mutual fund, you are buying shares of a fund that owns a basket of assets. The fund is the wrapper. The holdings inside the fund are the exposure.

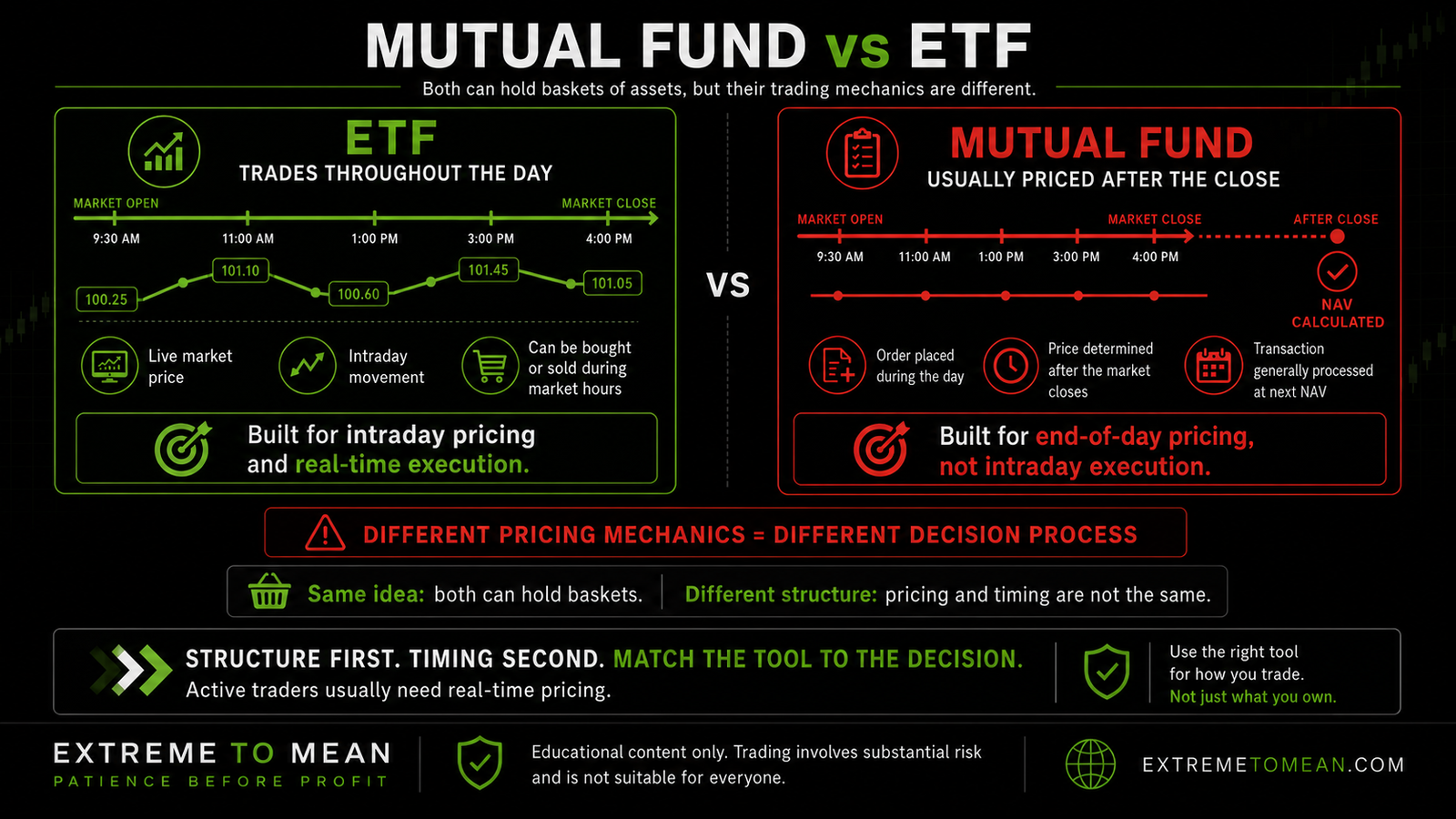

That makes mutual funds similar to ETFs in one broad way: both can give exposure to a basket. But the structure and trading mechanics are different. If you just finished learning what an ETF is, the key difference is that an ETF trades throughout the day like a stock, while a mutual fund is usually priced after the market closes.

That timing difference changes how the product is used.

Mutual Funds Are Priced Once Per Day

One of the biggest differences between mutual funds and ETFs is pricing.

A stock trades throughout the day. An ETF also trades throughout the day. Their prices can move minute by minute while the market is open. Traders can see live bid and ask prices, enter orders during the session, and manage decisions around intraday movement.

A traditional mutual fund works differently.

Most mutual funds are priced once per trading day after the market closes. That price is called the net asset value, or NAV. NAV is the value of the fund’s assets minus liabilities, divided by the number of fund shares outstanding.

In plain English, the fund calculates what its basket is worth after the market close, then uses that value to price fund transactions for the day.

That means if you place an order to buy or sell a mutual fund during the trading day, you usually do not know the exact execution price at the moment you place the order. The transaction is generally completed at the next calculated NAV.

This is not a flaw. It is simply how the product is structured.

But for active traders, that structure matters. Active trading often depends on timing, price location, intraday movement, and defined execution. A product priced once per day does not fit that style the same way a stock, ETF, or futures contract might.

Why Active Traders Rarely Center on Mutual Funds

Active traders usually need instruments that can be watched, entered, exited, and managed during the trading session. They may care about intraday structure, support and resistance, momentum, volatility, liquidity, spreads, and precise risk levels.

Mutual funds are not built for that kind of decision-making.

Because mutual funds are typically priced after the close, they do not offer the same intraday execution framework. A trader cannot usually say, “I want to enter at this exact intraday price, place my stop near this exact level, and adjust if the market rejects.” The product is not designed around that kind of active order management.

That is why Extreme to Mean content does not center on mutual funds. The site focuses more on market mechanics, context, location, setup quality, and risk decisions that active traders can evaluate in real time or near real time. Mutual funds may still be important in the broader investing world, but they are not usually the right teaching vehicle for intraday trade execution.

This distinction connects directly to the difference between trading and investing. A mutual fund may fit a long-term allocation decision, retirement account decision, or portfolio construction decision. That is different from using a chart to evaluate a specific trade setup with defined entry, invalidation, and risk.

The mistake is not using a mutual fund. The mistake is confusing the purpose of the tool.

The Beginner Confusion: Basket Does Not Mean Same Product

Beginners often hear that mutual funds and ETFs both hold baskets of assets, then assume they are basically the same. That assumption is understandable. Both can offer exposure to many holdings through one product. Both may track an index or follow a professional strategy. Both may be used by investors who want diversified exposure.

But “basket” does not mean “same mechanics.”

A mutual fund and an ETF may hold similar assets, but the trading experience can be different. The ETF has an intraday market price. The mutual fund usually has an end-of-day NAV. The ETF may be bought or sold during market hours like a stock. The mutual fund order is typically processed at the fund’s next calculated price.

That difference matters because process depends on mechanics.

If your decision requires intraday timing, you need a product that supports intraday timing. If your decision is about long-term exposure, automatic contributions, or portfolio allocation, intraday price movement may not be the main focus. The product should match the decision being made.

A beginner who does not understand this may look at a mutual fund chart and treat it like a day trading vehicle. That can lead to confusion because the chart may show historical daily values, not a live tradable intraday market in the same way as a stock or ETF.

A better trader asks, “Does this product match the decision I am trying to make?”

That question is simple, but it prevents a lot of confusion.

Structure and Timing Come Before Opinion

It is easy to turn financial products into opinions. Some people prefer mutual funds. Some prefer ETFs. Some prefer individual stocks. Some trade futures. But preference is not the first question a beginner should ask.

Structure comes first.

Before deciding whether a product fits your process, you need to know how it works. How is it priced? When does it trade? What does it hold? What kind of exposure does it provide? Can you manage risk in the way your decision requires?

Timing comes next.

A mutual fund priced once per day does not give the same timing control as an ETF trading throughout the session. That does not make it useless. It simply means it is designed for a different kind of decision.

This is where patience matters. Beginners often want to rush from product names to action. They hear about a fund, ticker, sector, or market theme and immediately start thinking about buying or selling. But Extreme to Mean is built around slowing that process down.

A product should not earn your attention just because it is familiar. It should earn your attention because you understand what it is, how it behaves, and whether it fits the decision in front of you.

For active trading, that usually means the trader needs tradable price action, clear location, and risk that can be defined before acting. Those ideas become more important in the deeper market context lessons, but the foundation starts with knowing the instrument.

A Simple Mutual Fund Decision Filter

A beginner does not need to memorize every mutual fund detail on day one. But they should know enough to avoid mixing up products that serve different purposes.

Before using or evaluating a mutual fund, ask:

- What does this mutual fund hold?

- Is it actively managed or designed to track an index?

- Is the purpose long-term exposure, income, allocation, or something else?

- How often is it priced?

- Will my order execute at a known intraday price or the next calculated NAV?

- Does this product match an investing decision or an active trading decision?

- Am I choosing this because I understand it, or because the name sounds familiar?

The better question is not, “Is this mutual fund good?”

The better question is, “What job is this product built to do, and does that job match the decision I am making?”

That question keeps the focus where it belongs. It turns the product from a label into a tool. It also helps beginners avoid forcing active trading logic onto a product that was not designed around active trading mechanics.

If you are still organizing the basic differences between products, the clean next step is to start with the beginner trading path and build the instrument map in order before moving into more advanced decision-making.

Final Thought

A mutual fund is a professionally managed basket of assets, but it is usually not an active trading vehicle. It is commonly priced once per day after the market closes, which makes it structurally different from stocks and ETFs that trade throughout the day.

That difference is not about better or worse. It is about fit.

The trader’s job is to understand the product before using it, match the tool to the decision, and avoid reacting to names, themes, or charts without knowing the mechanics underneath.

Educational content only. Trading involves substantial risk and is not suitable for everyone.