Most traders are introduced to the market through opportunity. They learn to recognize patterns, identify direction, find entries, and imagine where price could travel. The entire process naturally points their attention toward what they might gain.

Risk management usually arrives later.

It is treated as the less exciting part of trading: choose a stop, reduce the size, and try not to lose too much. That makes risk sound like an administrative task attached to the real work of finding trades.

In practice, risk management is the real work.

The trader’s job is not simply to find opportunities. It is to decide which opportunities justify exposure, how much uncertainty can be accepted, and whether one outcome could damage the decisions that follow.

That is why this lesson belongs within the broader trader psychology lessons. Thinking like a risk manager is not only about account math. It is a way of making decisions before hope, fear, urgency, and open profit or loss begin influencing the process.

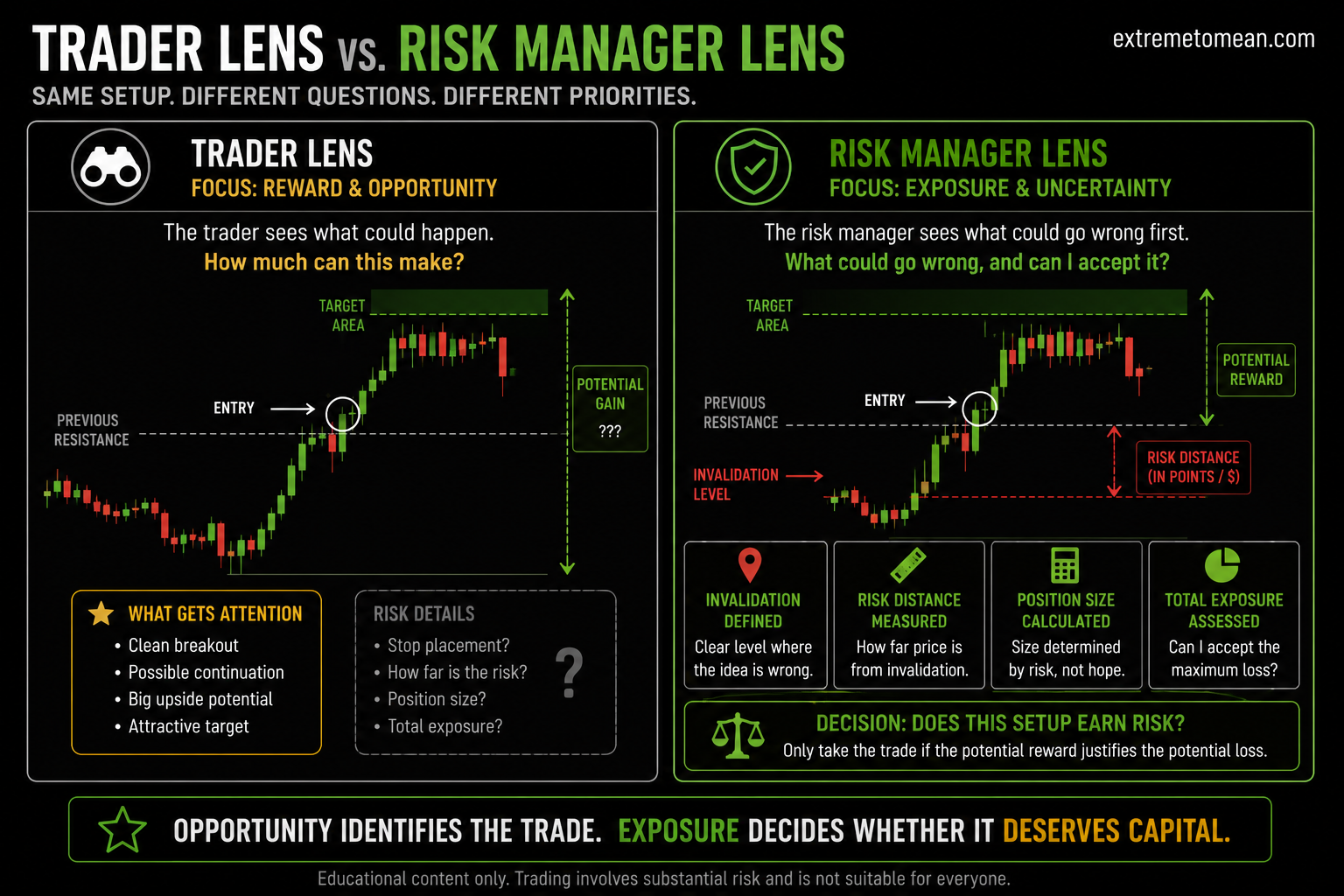

The Trader Sees Opportunity; the Risk Manager Sees Exposure

A trader and a risk manager can look at the same chart and focus on very different things.

The trader may see:

- A clean entry

- A familiar setup

- A possible breakout

- A strong directional move

- An attractive target

- A chance to recover a previous loss

The risk manager sees additional questions:

- Where is the idea invalidated?

- How far is the entry from that point?

- How much could be lost if the trade fails?

- Does volatility make the planned stop realistic?

- Is the position size appropriate for the uncertainty?

- Could one bad fill or fast move create more exposure than expected?

- Would the trader remain emotionally stable after the loss?

The risk manager is not trying to eliminate risk. That is impossible in trading.

The goal is to understand the risk well enough to make a deliberate choice about whether to accept it.

This changes how a setup is evaluated. An opportunity may look attractive but require a stop that is too wide for the planned size. Another may have a manageable stop but very little realistic room to the target. A third may be structurally sound but appear during a news event that makes execution less predictable.

The setup may still be interesting. It simply may not deserve capital under those conditions.

Thinking like a risk manager first does not prevent the trader from acting. It prevents action from occurring before exposure has been understood.

Why Reward-First Thinking Feels So Natural

Traders do not begin with reward because they are careless. They begin there because reward is the part of the trade that creates excitement.

A possible winning trade offers relief, progress, validation, or the chance to repair a difficult day. Once the trader imagines that outcome, the setup begins to feel more important.

The mind can then work backward to justify the entry.

The target looks obvious. The signal appears clean. The stop can be figured out later. The size feels acceptable because the trade looks likely to work.

This reasoning feels especially convincing when price is already moving. Speed creates urgency, and urgency makes unfinished decisions feel complete.

The trader may think:

- “I need to enter before it leaves.”

- “I will use a small stop once I am in.”

- “I can manage it manually.”

- “This setup is too clean to miss.”

- “I will reduce the size if it goes against me.”

- “I only need one good trade.”

Each statement postpones the risk decision until after exposure has already been created.

That is the critical mistake.

Once the trade is open, the trader is no longer evaluating the same situation from a neutral position. Every movement now affects account balance, emotion, and the desire to be right.

A plan that was unclear before entry rarely becomes clearer afterward. It usually becomes more flexible in exactly the wrong way.

This is why the trade is not ready until the risk is clear. Risk cannot be treated as an inconvenience that will be solved once the market cooperates.

Exposure Changes Decision Quality

Every trade creates two forms of exposure.

The first is financial. This includes the position size, stop distance, slippage, volatility, and total amount that could reasonably be lost.

The second is psychological. This is the pressure created by having money at risk.

Those two forms of exposure are connected.

A position that is too large can make normal price movement feel threatening. A trader who planned to wait for structural invalidation may suddenly exit during an ordinary pullback. Another may widen the stop because accepting the planned loss now feels unbearable.

The chart has not necessarily changed. The trader’s capacity to follow the chart has.

Undefined or excessive risk commonly leads to:

- Watching profit and loss instead of market structure

- Moving a stop to avoid accepting the loss

- Exiting early because normal movement feels dangerous

- Adding to a losing position without a defined plan

- Taking another trade immediately to recover

- Lowering setup standards after a loss

- Holding longer because the loss has become emotionally difficult to realize

This is why the correct risk amount cannot be determined only by what the account can technically withstand.

The trader also has to consider what they can manage without losing decision quality.

A $200 loss may be financially small relative to one account and still create enough emotional pressure to damage the next several decisions. A much smaller planned loss may be more appropriate while the trader is still learning to follow the process under uncertainty.

The purpose of risk management is not to make losing comfortable. It is to prevent one loss from becoming a chain of increasingly poor decisions.

The lesson to protect your next decision begins here. Exposure should be controlled so that the trader can still evaluate the next opportunity instead of reacting to the previous result.

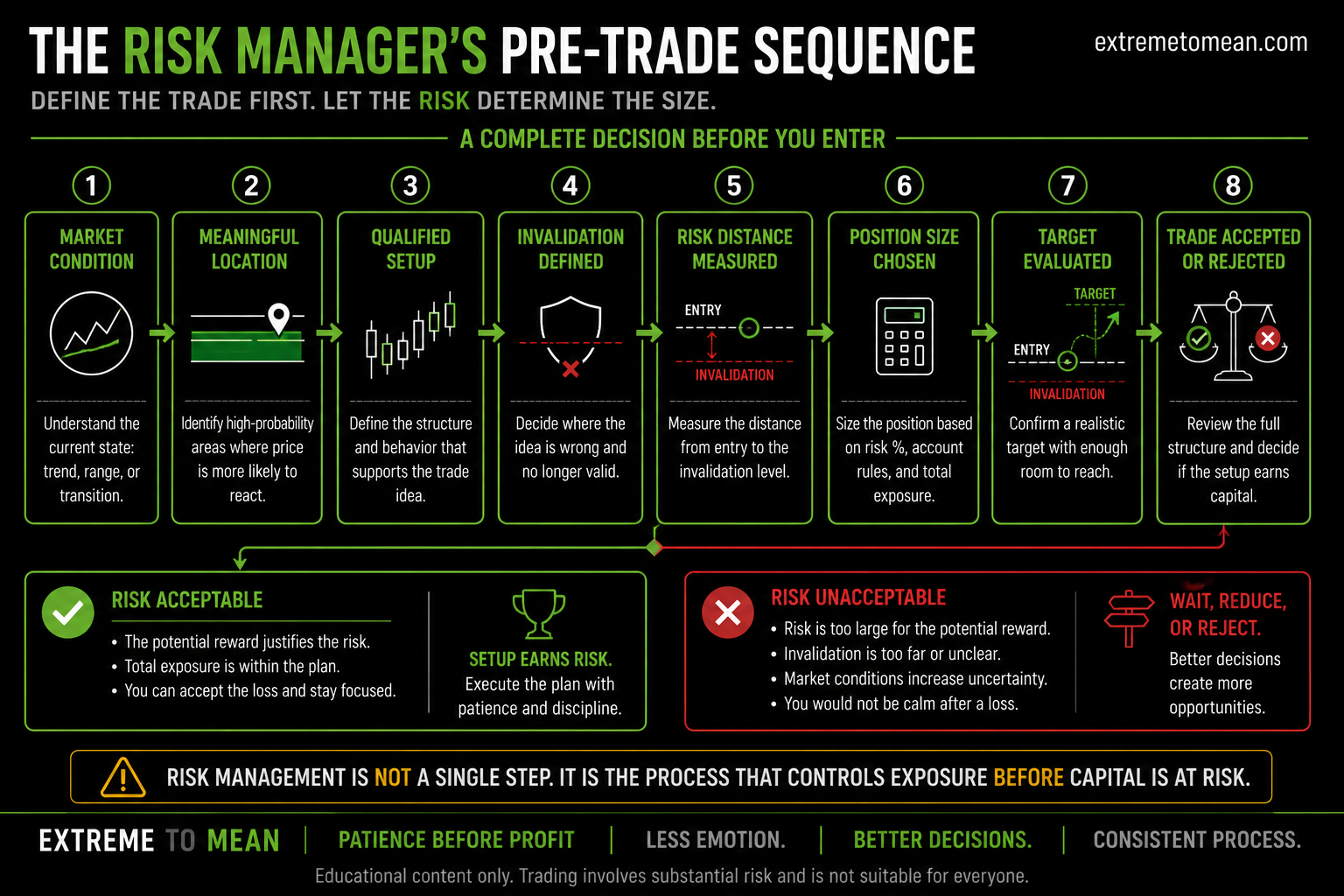

Risk Management Begins Before the Trade

Risk management is often confused with stop placement. A stop is important, but it is only one part of the process.

Risk begins with trade selection.

A trader manages risk when they reject an unclear market, avoid entering from poor location, reduce size during unstable conditions, or decide that a setup lacks enough room to justify the exposure.

In that sense, patience is a risk-management tool.

Waiting for better location can create a clearer invalidation point. Waiting for the setup to finish forming can reduce uncertainty. Standing aside during poor conditions can avoid exposure that never needed to exist.

The process should normally move in this order:

- Understand the market condition.

- Identify the location.

- Define the setup.

- Determine where the idea is wrong.

- Measure the distance from entry to invalidation.

- Choose the position size.

- Evaluate the realistic target.

- Decide whether the complete structure deserves risk.

Many traders reverse steps four through six. They choose the size they want to trade, then place the stop wherever the resulting dollar loss feels acceptable.

That allows the desired position size to control the trade structure.

A risk manager does the opposite. The market structure defines the invalidation point, and the invalidation distance helps determine the size.

The trader may discover that the correct size is smaller than expected. They may also discover that no reasonable size makes the trade attractive enough to take.

That is not a failure to find an entry. It is a successful risk decision.

Good location remains important because where you enter matters more than what you predict. Better entries can create cleaner invalidation, more realistic targets, and less pressure to interfere after the trade begins.

The Risk Manager’s Pre-Trade Questions

A trader does not need an elaborate risk model before every entry. They do need clear answers to a few practical questions.

What is the total exposure?

Include the planned size, stop distance, potential slippage, and any additional positions connected to the same market idea.

Two trades in closely related instruments may look separate while creating similar directional exposure.

Where is the idea wrong?

Identify the price level, structural failure, or market behavior that invalidates the reason for entering.

The answer should not be “when the loss becomes uncomfortable.”

Is the stop based on structure or on the amount I want to lose?

The structure should determine where the idea fails. Position size should then adjust to keep the total exposure within the plan.

Forcing a tight stop onto a trade that needs more room does not create lower risk. It may create a poorly structured trade with a higher chance of being exited by normal movement.

What could make the actual loss larger?

Consider fast markets, gaps, thin liquidity, scheduled news, wider spreads, and slippage.

A stop order can help manage risk, but it cannot guarantee the exact exit price.

Is the target realistic?

The target should reflect market structure and available room, not simply produce an attractive ratio on paper.

A trade that appears to offer three-to-one reward is not automatically well constructed if the target requires price to move through several major obstacles.

Can I accept the loss without changing my behavior?

This is not a question about enjoying the loss. It is a question about whether the planned outcome would cause the trader to abandon the process.

Would the loss create an urge to increase size, chase, revenge trade, or ignore the next setup’s standards?

What happens after the trade?

Know whether the plan permits another trade, requires a pause, or ends the session after a particular loss or rule violation.

The better question is not:

How much can I make if this works?

It is:

What can go wrong, what will it cost if it does, and will I still be able to make a clear decision afterward?

That question does not make trading pessimistic. It makes the decision complete.

Final Thought

Thinking like a trader begins with possibility. Thinking like a risk manager begins with consequence.

Both perspectives matter, but the order matters more.

Before looking at the potential reward, define the exposure. Before choosing the position size, define where the idea is wrong. Before entering, decide whether the loss would leave the account and the trader capable of continuing with discipline.

Risk management is not what traders do after finding a setup. It is how they decide whether the setup deserves capital at all.

When the exposure is unclear, the trade is unclear. The cleaner decision is to wait until the risk can be explained, measured, and accepted.

Traders who repeatedly enter before answering these questions should begin with the guidance on having unclear risk and make risk definition part of the pre-trade process.

Educational content only. Trading involves substantial risk and is not suitable for everyone.