New traders usually calculate a trade in the simplest possible way. They subtract the entry price from the exit price, multiply the difference by the position size, and treat the answer as the result.

That calculation is useful, but it may not be complete.

Trading requires access to markets, order processing, execution, and sometimes real-time data or specialized software. Some of those services create direct charges. Other costs are built into how orders interact with available buyers and sellers.

Individually, many of these costs can look small. The problem appears when the trader ignores them, trades frequently, uses large size, or targets moves that are only slightly larger than the cost of participation.

This lesson belongs in the broader Basics learning path because understanding price and orders also requires understanding what it costs to turn an idea into an actual position.

The Visible Result Is Not Always the Final Result

Imagine a trader buys an instrument at $100 and later sells it at $101.

At first glance, the trade made $1 per share. With 100 shares, the visible difference is $100.

But the final account result may also reflect:

- Commission charged when entering

- Commission charged when exiting

- Exchange or regulatory fees

- The difference between the bid and ask

- Slippage between the requested and actual fill

- Platform or data costs associated with trading

- Financing or interest charges in certain positions

Not every trade includes every cost. Some brokers advertise commission-free trading for specific products, while futures, options, or specialized routes may use per-contract or per-order pricing. Some charges appear directly on the account statement, while others are reflected in the fill price.

That is why a trader should distinguish between:

- Gross result: The price-based result before trading costs.

- Net result: What remains after applicable costs are included.

The difference may be minor on one trade. Across dozens or hundreds of trades, it can become a meaningful part of performance.

Cost awareness does not mean avoiding all trading activity. It means understanding the complete decision before assuming that every visible price move represents usable opportunity.

Commissions: The Direct Charge for Trading

A commission is a direct charge associated with executing a transaction.

The commission structure depends on the broker and instrument. It may be charged:

- Per order

- Per share

- Per options contract

- Per futures contract

- Per side of the trade

- As part of a bundled pricing arrangement

The phrase per side matters. Entering a position is one side, and exiting is another. A quoted commission of $2 per contract per side would therefore create a $4 round-trip commission for one contract before other applicable fees.

A round trip means the complete entry and exit of a position.

For example, a futures trader may see:

- Entry commission

- Entry exchange and clearing fees

- Exit commission

- Exit exchange and clearing fees

The trader may think of this as one trade, but the cost structure recognizes two transactions.

Commission-free does not necessarily mean cost-free. A broker may charge no stated commission on certain stock or ETF trades while the trader still experiences spread, slippage, subscription costs, or other account-related charges.

The correct question is not simply, “Does this broker charge a commission?”

A better question is:

What is the complete round-trip cost for the instrument, size, and order process I intend to use?

Fees: The Smaller Charges That Add Up

Fees are charges associated with the systems and organizations involved in processing market activity.

Depending on the market and account, they may include:

- Exchange fees

- Clearing fees

- Regulatory fees

- Transaction fees

- Data-subscription fees

- Platform fees

- Routing fees

- Exercise or assignment fees for options

- Financing or margin interest

- Withdrawal or account-service fees

Some fees are tiny and assessed only under particular circumstances. Others may be a regular part of every transaction.

A futures trader, for example, may pay exchange and clearing fees alongside the broker’s commission. An options trader may pay a per-contract charge and face separate costs if contracts are exercised or assigned. A trader using professional market data may pay a monthly subscription whether they place one trade or one hundred.

These charges should not be treated as hidden mysteries. A reputable broker normally publishes a pricing schedule, though the schedule may take time to understand.

Before trading a new product, the trader should review the applicable costs rather than relying only on an advertised headline rate.

This is especially important when comparing instruments. Stocks, ETFs, futures, and options may appear similar on a chart, but their contract structures and trading costs are different. The basic differences between stocks, ETFs, futures, and options provide the foundation for understanding why one cost model cannot be applied to every product.

The Spread: A Cost Built Into the Quote

The spread is the difference between the highest current bid and the lowest current ask.

The bid represents the highest displayed price a buyer is currently willing to pay. The ask represents the lowest displayed price a seller is currently willing to accept.

If the quote is:

- Bid: $100.00

- Ask: $100.05

the spread is five cents.

A trader who buys immediately with a market order may receive a fill near the ask. If they immediately sell with another market order and conditions have not changed, they may receive a fill near the bid.

That means the position can begin with a small negative difference before the broader market moves at all.

This does not mean the spread is a separate invoice sent by the broker. It is an execution cost created by the difference between available buying and selling prices.

Spreads are often narrower in highly liquid markets and wider when:

- Trading activity is thin

- Volatility is elevated

- News is being released

- The market is closed or outside its most active session

- The instrument has fewer participants

- Price is moving too quickly for quotes to remain stable

The spread matters more when the trader’s target is small. A five-cent spread may be minor inside a multi-dollar move, but significant if the trader is attempting to capture only ten cents.

Readers should understand what bid, ask, and spread mean before assuming the chart’s last price is the exact price available for both buying and selling.

Slippage: When the Fill Is Different From the Expectation

Slippage occurs when the actual execution price differs from the price the trader expected.

Suppose a trader submits a market order while the ask is $100.05. By the time the order reaches the available market, the best sellers may have been filled by other participants. The trader could receive $100.07, $100.10, or multiple prices if the order is larger than the quantity available at one level.

Slippage can occur on both entry and exit.

It is more likely when:

- Price is moving rapidly

- Available liquidity is limited

- The position is large relative to the available orders

- Important news is being released

- The market gaps

- A stop order is triggered during a fast move

- The instrument trades infrequently

Slippage is not always negative. A limit order can occasionally receive price improvement, and an execution may occur at a better price than expected. But traders should not build a plan that assumes favorable slippage.

The practical lesson from why fill prices can be different is that an order controls an instruction, not the complete market environment in which the order will be executed.

A stop can define a planned exit area, but it cannot guarantee the exact fill price during every condition.

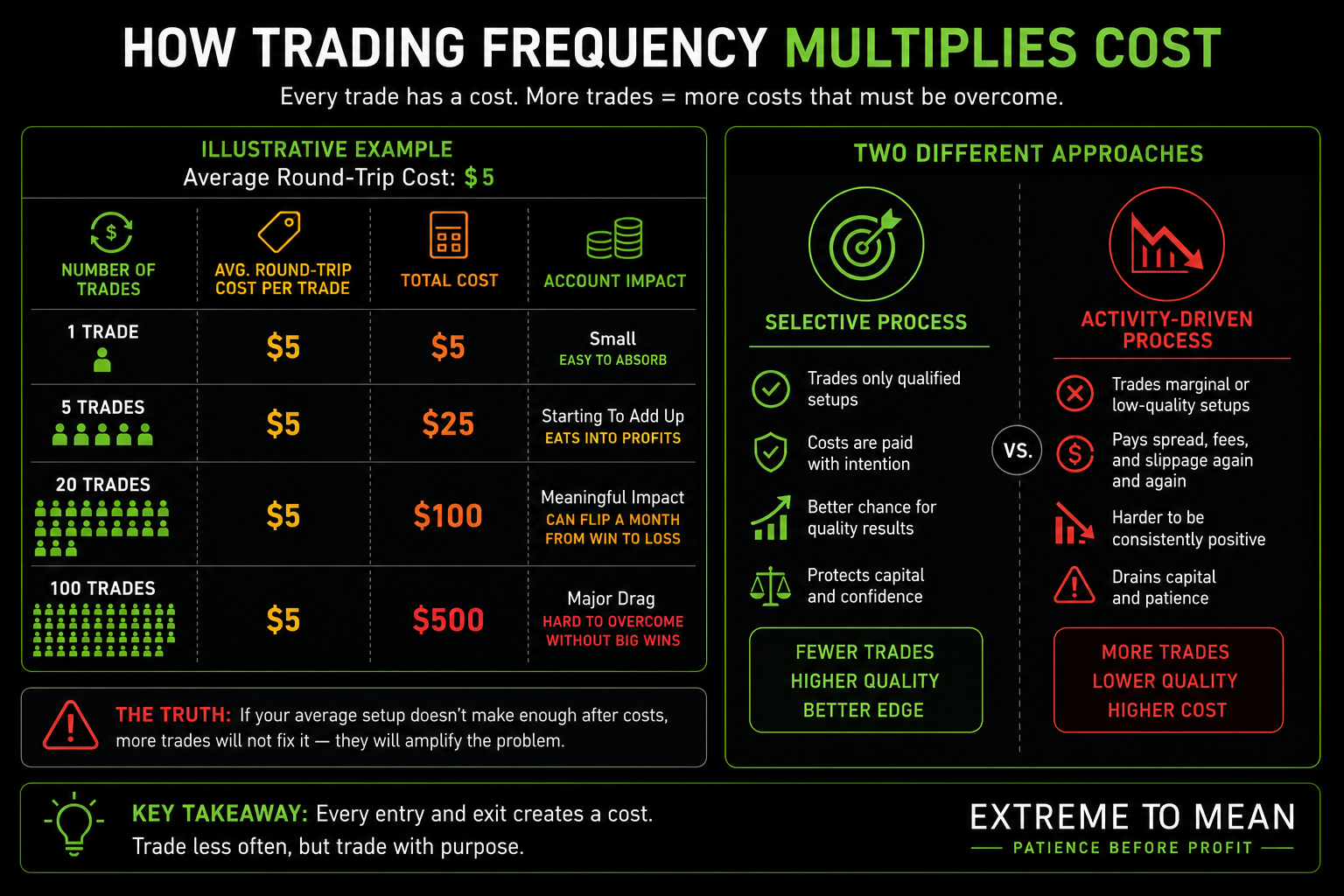

Small Costs Become Larger Through Repetition

The cost of one trade can appear unimportant. Frequency changes the calculation.

Assume a trader’s average round-trip cost is $5 after commissions, fees, and normal execution differences.

That would equal:

- 1 trade: $5

- 5 trades: $25

- 20 trades: $100

- 100 trades: $500

The cost does not become unreasonable merely because it is repeated. The problem is that every additional trade must overcome its own participation cost before contributing positively to the account.

This makes frequent low-quality trading especially expensive.

A trader may take several nearly identical trades during a choppy session, lose very little on price movement, and still create a noticeable account loss through repeated costs. The chart may appear to have gone nowhere, but the account has paid for each entry and exit.

This is one reason more activity is not automatically more productive. A trade should not be taken merely because its visible price risk appears small. The total decision includes the cost of participation and the possibility that several small decisions will accumulate.

Patience can therefore have an economic value. Rejecting a weak trade avoids not only its market exposure, but also the cost of entering and exiting an idea that never earned attention.

Costs Matter Relative to the Trade

A $5 round-trip cost cannot be judged in isolation.

Its importance depends on:

- Position size

- Expected price movement

- Average target

- Holding period

- Instrument

- Trading frequency

- Typical spread

- Volatility

- Order type

- Available liquidity

For a longer-duration trade seeking a substantial move, a modest transaction cost may represent a small part of the planned opportunity.

For a scalper seeking a very small move, the same cost may represent a large portion of the target.

Consider two hypothetical trades:

Trade A

- Planned gross target: $500

- Estimated total cost: $5

Trade B

- Planned gross target: $15

- Estimated total cost: $5

The same cost affects each decision very differently.

This does not automatically make Trade A better. It may require more risk, more time, or a less realistic target. The example only shows that costs must be evaluated relative to the trade structure.

A strategy that looks effective before costs can behave differently after realistic execution is included. That is why paper calculations and backtests should account for commissions, fees, spread, and reasonable slippage rather than assuming every trade enters and exits at a perfect displayed price.

A Practical Pre-Trade Cost Check

A beginner does not need to calculate every possible penny before each order. They should understand the recurring costs of their chosen instrument and recognize when conditions may make execution more expensive.

Before trading, ask:

What is the normal round-trip commission?

Include both entry and exit rather than looking at only one side.

Which additional fees apply?

Review exchange, regulatory, clearing, data, platform, and product-specific charges.

What is the current spread?

Compare it with the trade’s intended target. A spread that is unusually wide may signal thin or unstable conditions.

How much slippage is realistic?

Consider current volatility, liquidity, scheduled news, order size, and whether a market or stop order may be used.

How frequently am I trading?

A small cost repeated many times may become more important than expected.

Is the intended move large enough to justify participation?

This is not a promise that the target will be reached. It is a question about whether the potential opportunity is meaningful relative to the cost and uncertainty.

Am I taking this trade because it qualifies—or because I want activity?

The better question is:

After realistic trading costs are included, does this setup still deserve capital and attention?

If the answer is unclear, the trader may need a better location, a cleaner setup, a more suitable instrument, or no trade at all.

Final Thought

The real cost of a trade extends beyond the visible difference between entry and exit.

Commissions and fees create direct charges. The spread creates a cost between available buying and selling prices. Slippage can change the execution from what the trader expected. Repeated activity can multiply all of them.

None of these costs means trading should be avoided. They mean trading should be evaluated honestly.

A complete process asks not only whether price may move, but whether the potential move justifies the structure, exposure, and cost required to participate. The trader’s job is to evaluate the full decision—not react to every available button or every small movement.

Readers who want a practical way to slow down that decision can use the free trading tools and checklists to evaluate setup quality before paying the cost of participation.

Educational content only. Trading involves substantial risk and is not suitable for everyone.