Most beginners assume that if a chart shows a price, that is the price they will get. They see price moving near a level, press buy or sell, and expect the trade to happen exactly where they were looking. Sometimes the fill is close. Other times, the final price is different.

That difference can feel confusing at first.

The platform may show one price. The quote may show another. The order ticket may fill somewhere slightly different. In fast, thin, or volatile conditions, the difference can become more noticeable. That difference is called slippage.

At Extreme to Mean, this belongs in The Basics lesson library because slippage connects several beginner concepts into one practical lesson: liquidity, bid, ask, spread, order type, and execution quality. A trader does not need to fear slippage, but they do need to understand it before assuming every order will fill exactly as expected.

Slippage Means Expected Price vs. Actual Fill Price

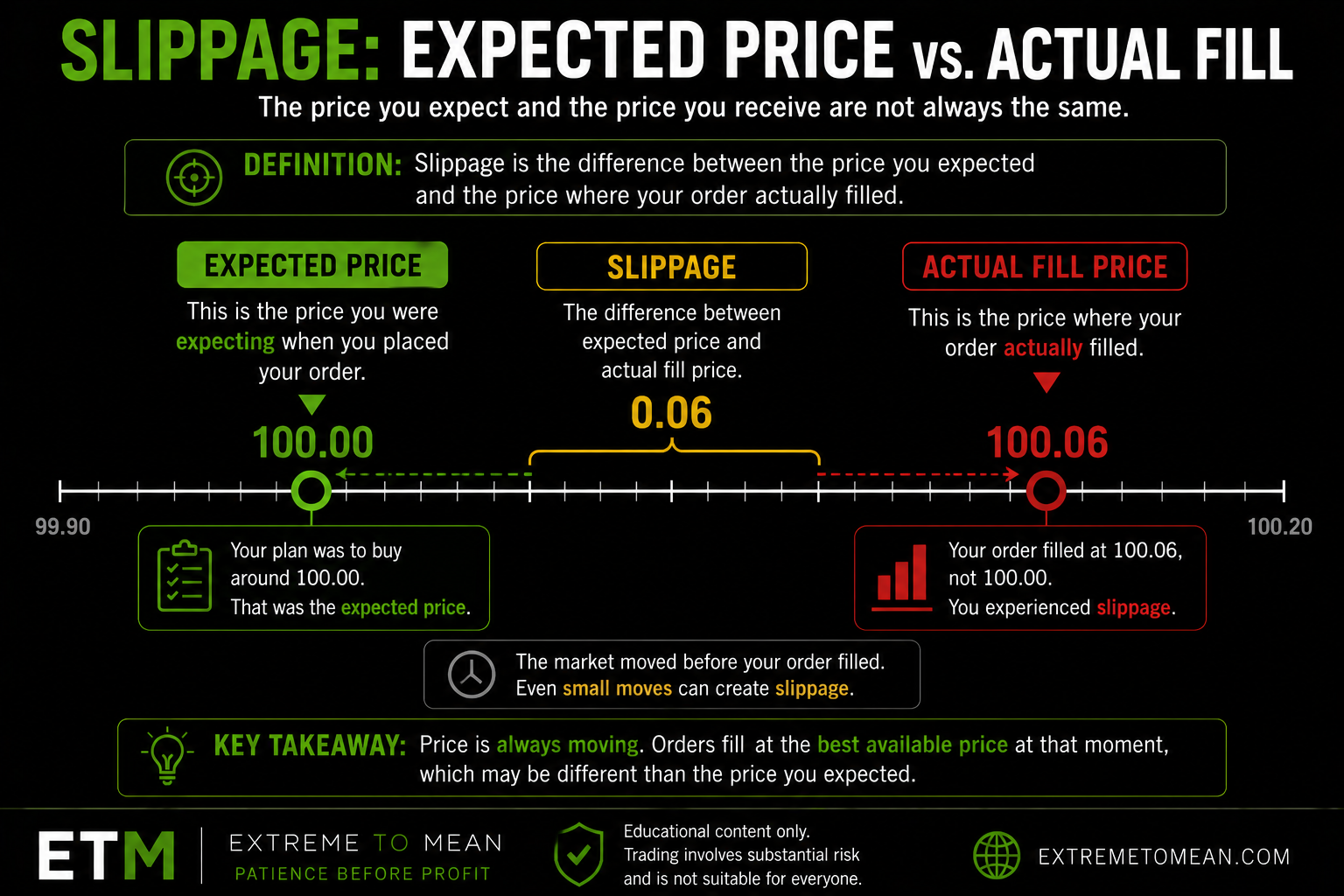

Slippage happens when an order fills at a different price than the trader expected.

For example, imagine a trader sees a stock trading near $100.00 and sends a buy order expecting to enter around that price. If the order fills at $100.04, the trader experienced four cents of slippage. If the trader sends a sell order expecting $100.00 and fills at $99.96, that is also slippage.

The idea is simple: expected price and actual fill price were not the same.

Slippage can happen on entries and exits. It can happen when buying, selling, going long, going short, exiting a winner, or exiting a loser. It can be small enough to barely notice, or large enough to change the quality of the trade.

Slippage is not always a sign that something went wrong. It is part of live-market execution. Markets are constantly changing. Quotes update. Orders get filled. Liquidity appears and disappears. When a trader sends an order, that order interacts with the market that exists at that moment, not the market the trader hoped would still be there.

This is why the earlier lesson on what bid, ask, and spread mean matters. The chart may show price movement, but the actual fill depends on where buyers and sellers are available when the order reaches the market.

Why Slippage Happens

Slippage usually happens because the market changes between the price the trader expected and the price where the order is executed.

Sometimes the change is tiny. In a liquid market with a tight spread, the expected price and fill price may be very close. In other conditions, the market can move before the order is completed. That can create a fill that is worse than expected.

Several conditions can make slippage more likely:

- Fast price movement

- Thin liquidity

- Wide bid-ask spreads

- News events

- Market opens or closes

- Extended-hours trading

- Large orders relative to available liquidity

- Stop orders triggering during sharp moves

The common thread is that available buyers and sellers may not be sitting exactly where the trader expected them to be.

If a trader sends a market buy order, the order seeks available sellers. If sellers at the expected price are gone or there are not enough of them, the order may fill at a higher price. If a trader sends a market sell order, the order seeks available buyers. If buyers at the expected price are gone or not deep enough, the order may fill lower.

This is why slippage is connected to liquidity. Liquidity describes how easily buyers and sellers can trade without causing a large price disruption. The lesson on what volume and liquidity mean explains that activity and tradability are related, but not the same.

High activity does not always mean clean execution. A market can be busy and still difficult to trade cleanly if orders are moving quickly, spreads are widening, or available liquidity is being consumed.

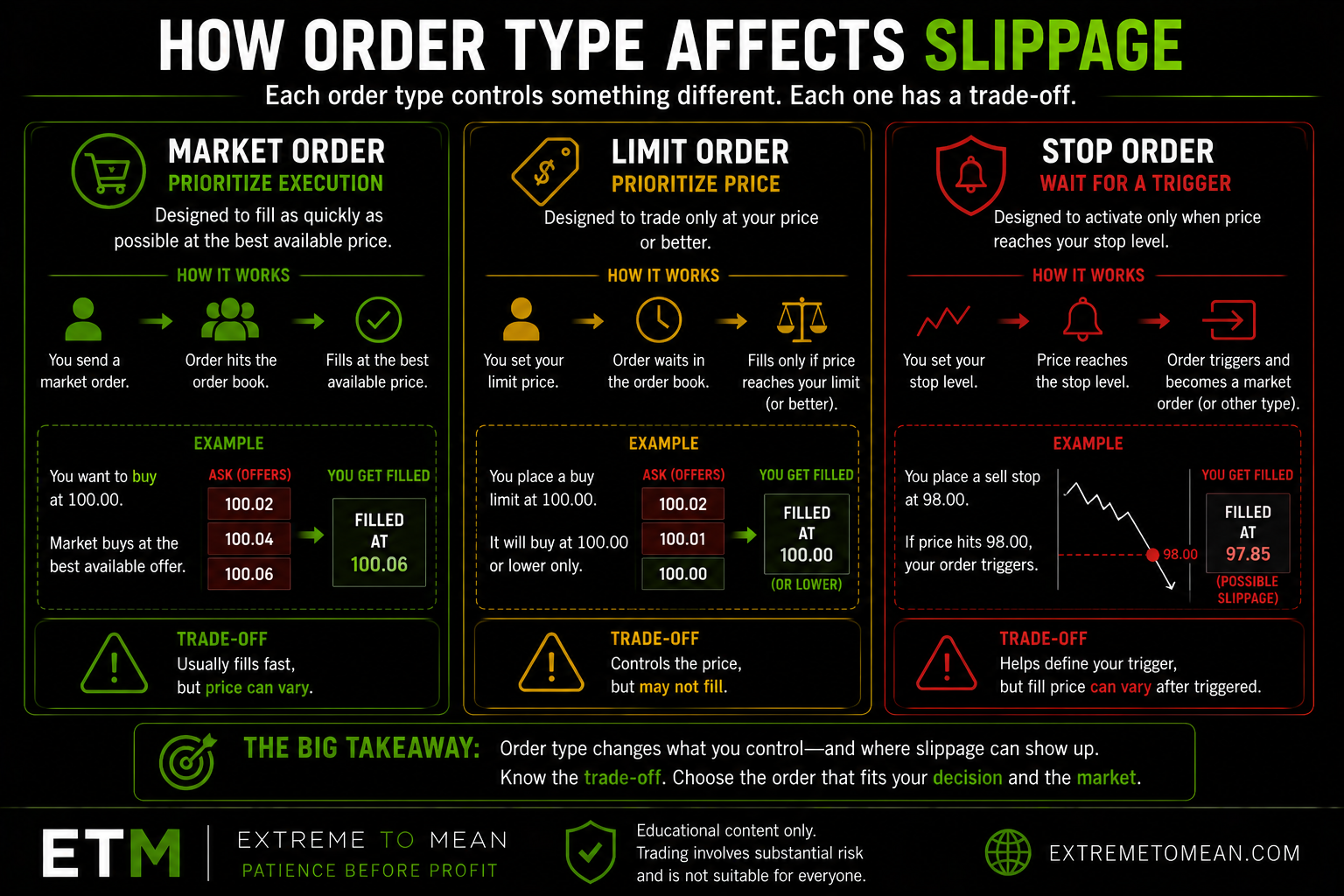

Market Orders and Slippage

Market orders are one of the most common places beginners experience slippage.

A market order tells the broker to execute as soon as possible at the best available price. That sounds simple, and it often is. But the tradeoff is that the trader prioritizes speed over exact price.

If the market is liquid and calm, a market order may fill close to the quote the trader saw. But if price is moving quickly, the best available price may change before the order is completed. The trader may get filled above the expected price when buying or below the expected price when selling.

This does not mean market orders are bad. It means market orders have a tradeoff.

The trader is saying, “I want execution now, and I accept that the fill price may vary.” That may be acceptable in some situations and unacceptable in others. The order type should match the decision, the market condition, and the trader’s risk tolerance.

The earlier article on market orders, limit orders, and stop orders explains this tradeoff directly. Market orders prioritize execution. Limit orders prioritize price. Stop orders wait for a trigger. Slippage becomes easier to understand once the trader knows what each order type is designed to control.

A beginner should not ask only, “Will this order fill?”

A better question is, “What price uncertainty am I accepting to get filled quickly?”

That question brings the trader closer to the real execution process.

Limit Orders and Slippage

Limit orders work differently because they set a price boundary.

A buy limit order says, “Buy at this price or lower.” A sell limit order says, “Sell at this price or higher.” Because of that, a limit order gives the trader more control over price than a market order.

That can help reduce unwanted slippage, but it creates a different tradeoff: the order may not fill.

For example, if a trader places a buy limit at $100.00, the order should not buy above $100.00. But if price does not trade there, or if there is not enough available liquidity when it does, the order may sit unfilled. The trader avoided paying more than planned, but they may miss the trade.

That is not a platform failure. That is the instruction doing what it was told to do.

A limit order can be useful when price discipline matters. It allows the trader to decide in advance what price is acceptable. But a limit order does not guarantee participation. The trader may need to choose between waiting for a better price, adjusting the order, or passing on the trade.

This is part of decision quality. A trader who says, “I only want this trade if I can get this price or better,” is making a different decision from a trader who says, “I want in now at the best available price.”

Neither instruction is automatically right. The point is to understand the tradeoff before placing the order.

Stop Orders and Slippage

Stop orders can also involve slippage, especially in fast markets.

A stop order uses a trigger price. When price reaches that trigger, the order becomes active. Depending on the type of stop order used, it may then become a market order or another order type. Many beginners do not understand that a basic stop-market order does not guarantee the exact stop price.

For example, imagine a trader owns a position and places a sell stop at $98.00. If price trades down to $98.00, the stop is triggered. But if the market is moving quickly and available buyers are below that level, the fill may occur at $97.90, $97.75, or another lower price.

The stop did not necessarily fail. It triggered. The fill depended on available liquidity after the trigger.

This is why stops are not magic shields. They are instructions. They can help define when a trader wants action to happen, but they cannot remove all execution risk. In a gap, a news shock, a thin product, or a fast selloff, the fill may be different from the stop price.

This does not mean traders should avoid learning stops. It means beginners should understand what a stop does and what it does not do. A stop can be part of risk management, but the trader still needs to think about liquidity, spread, volatility, and the possibility of a worse fill.

That is why the lesson on why the trade is not ready until the risk is clear matters. Risk is not only about where the trader wants to exit. It is also about whether the trader understands how that exit may actually execute.

Why Slippage Feels Worse Than Expected

Slippage often feels personal because it happens at the exact moment the trader is trying to act.

The trader makes a decision, sends the order, and sees a fill price that is worse than expected. That can create frustration, especially if the trader thought the chart price was the trade price. It can feel like the market moved on purpose, the platform was unfair, or the trader did something wrong.

Sometimes there may be an issue worth checking. But often, slippage is simply the result of live execution.

Markets do not freeze while a trader clicks. Buyers and sellers continue changing their orders. Quotes update. Spreads shift. Other traders may be acting at the same time. If the trader uses an order type that prioritizes execution, the final fill reflects the available market at that moment.

This is why slippage can be a dangerous emotional trigger. A trader may try to “make back” the difference immediately. They may chase the next move, widen risk without a plan, or blame the fill instead of reviewing the decision process.

A cleaner response is to evaluate.

Was the market fast? Was the spread wide? Was the order type appropriate? Was the product liquid enough? Was the trader trying to enter during news, the open, the close, or after-hours? Did the execution risk fit the trade idea?

Those questions do not remove frustration, but they turn frustration into useful review.

A Simple Slippage Filter Before You Trade

Before placing an order, a beginner should think about slippage as part of the execution plan.

Start with these questions:

- What price do I expect?

- What price would still be acceptable?

- Is the spread tight or wide?

- Is the product liquid enough for the order I am placing?

- Am I using a market order, limit order, or stop order?

- Am I trading during fast movement, news, the open, the close, or extended hours?

- What happens if the fill is worse than expected?

- Does this order type match what I am trying to control?

- Is the trade still valid if the fill is not perfect?

These questions do not guarantee a clean fill. They help the trader prepare for the reality that execution is not always exact.

The better question is not, “How do I avoid all slippage?”

The better question is, “Do I understand where slippage could happen, and does the trade still make sense if execution is imperfect?”

That is a more professional way to think. It keeps the trader grounded. It also reinforces a core Extreme to Mean principle: a setup earns attention before it earns risk. If the execution environment is messy, the trader does not have to force the trade.

For newer readers, the best next step is to start with the beginner trading path before moving deeper into execution, risk, and trade management.

Final Thought

Slippage is the difference between the price a trader expected and the price where the order actually filled.

It can happen because markets move, liquidity changes, spreads widen, or order types behave according to their instructions. It is especially important in fast, thin, volatile, or news-driven conditions.

Slippage is not something to fear blindly, and it is not something to ignore. It is part of trading execution. A trader who understands slippage can plan more clearly, choose order types more carefully, and avoid assuming that the chart price is always the fill price.

The better trader does not ask only, “Where do I want to trade?” The better trader asks, “How will this order execute, what could the fill look like, and does that still fit the risk I am willing to take?”

That is how slippage becomes part of a better trading process.

Educational content only. Trading involves substantial risk and is not suitable for everyone.