The word margin appears throughout trading platforms, brokerage agreements, and account dashboards. Traders see terms such as initial margin, maintenance margin, available margin, excess margin, and margin buying power.

Because these numbers appear next to order-entry controls, it is easy to treat them as risk limits. A platform may show that an account has enough buying power for several contracts, so the position can appear affordable.

That conclusion can be dangerously incomplete.

The broker’s question is:

Does this account meet the requirement to hold the position?

The trader’s question should be:

What happens to my account if this position moves against me?

Those are not the same question.

Before studying margin, a trader should understand how ticks, points, and contract value turn price movement into dollars. Margin controls access to that exposure. It does not replace the need to calculate it.

Margin Is a Requirement, Not the Purchase Price

When traders buy shares in a cash account, they generally pay the full purchase price. Buying 100 shares at $20 requires approximately $2,000, before trading costs.

Leveraged products operate differently.

A trader may be able to control a position whose total market exposure is much larger than the capital required to open it. The amount required by the broker or clearing system is called margin.

In futures, margin is often described as a performance bond. It is capital set aside to support the trader’s financial obligations while the position remains open. The trader does not purchase the underlying index, commodity, currency, or interest-rate instrument for its full value.

This creates an important distinction:

- Position value describes the market exposure being controlled.

- Margin requirement describes the capital required to hold that exposure.

- Trade risk describes the amount the trader expects to lose if the planned invalidation level is reached.

These values can be very different.

Suppose one futures contract represents $25,000 of notional market exposure. A broker may require only a portion of that amount as margin. That does not make the position a small position. It means the trader is controlling larger exposure with less capital committed upfront.

Margin makes leveraged exposure possible.

It does not make the underlying exposure disappear.

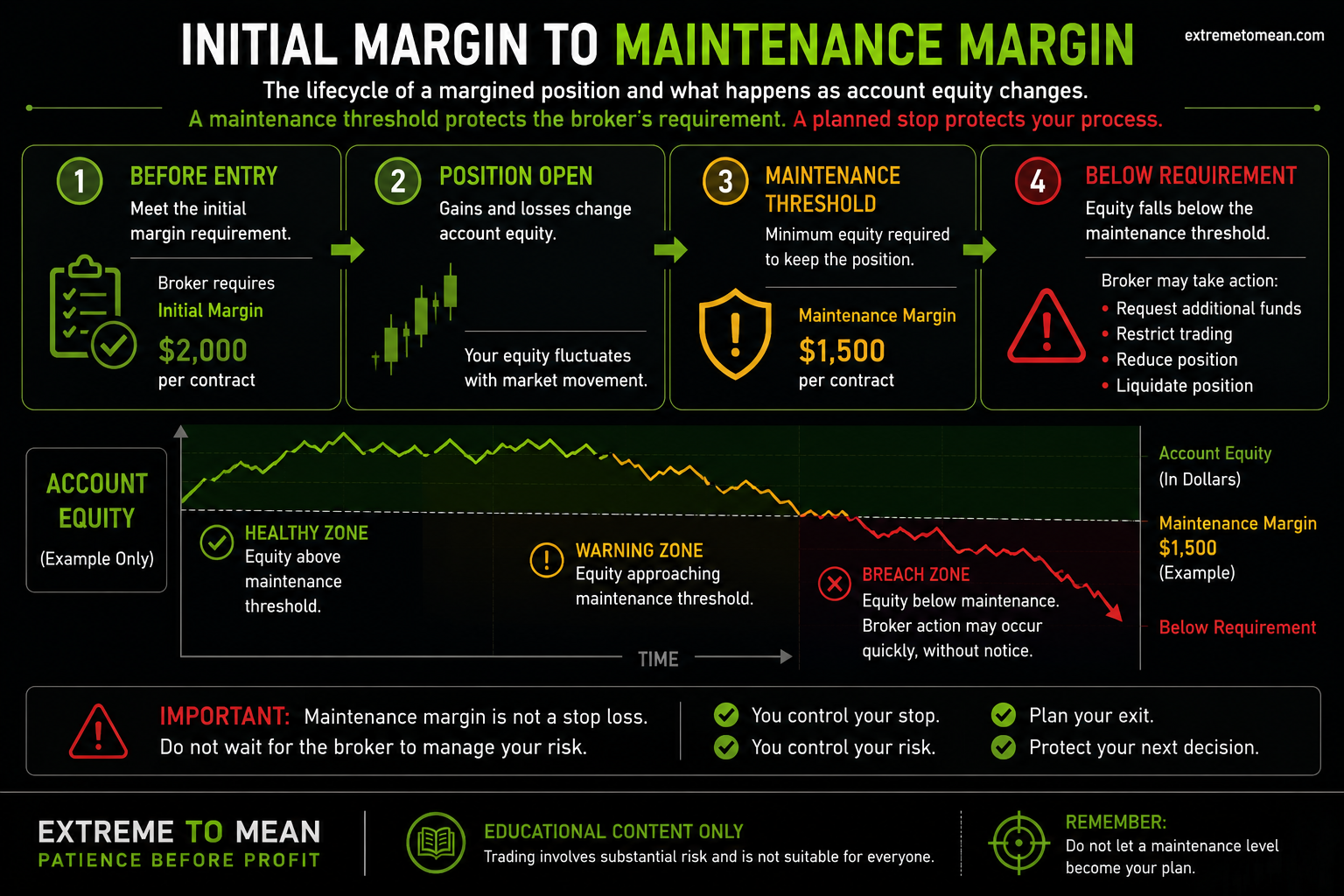

Initial Margin Opens the Position

Initial margin is the amount generally required to establish a leveraged position.

The exact terminology and calculation can vary by market, broker, clearing firm, account type, and regulatory structure. In futures trading, the exchange or clearing system establishes risk-based requirements, while a broker may impose additional requirements.

If the initial margin requirement is $2,000 per contract, an account may need at least $2,000 of qualifying capital to open one contract. Opening two contracts may require approximately $4,000, subject to the broker’s rules and any offsets or adjustments.

This number answers a narrow question:

How much qualifying capital is required to establish the position?

It does not answer:

- Where the stop should be placed

- How much the trade could lose

- Whether the setup is valid

- Whether the position matches the account

- Whether the market could gap beyond the intended exit

- Whether slippage could increase the loss

A trader can satisfy the initial margin requirement while still taking a poorly constructed trade.

The platform may accept the order. That does not mean the decision has earned risk.

Maintenance Margin Keeps the Position Open

Maintenance margin is the minimum account equity generally required to continue holding a leveraged position.

Once the trade is open, gains and losses affect account equity. If losses reduce the account below the applicable maintenance requirement, the broker may require additional funds, restrict the account, reduce the position, or liquidate it.

The exact response depends on the market and broker agreement. Traders should not assume they will always receive a traditional margin-call warning or enough time to make a new decision.

In a fast market, a broker may act to protect itself from further exposure.

This is why maintenance margin should not become a trader’s stop-loss plan. Waiting until the broker forces a reduction means the trader has surrendered control of the exit process.

A planned stop is based on market structure, invalidation, and acceptable dollar risk. A maintenance threshold is based on the financial requirements of carrying the position.

The trader should act long before the account reaches a forced-liquidation condition.

Futures Margin Can Change

Futures margin is not always a fixed number.

Requirements can increase when volatility rises, major events approach, liquidity becomes less reliable, or the exchange and broker determine that the product carries greater short-term risk. Brokers may also apply stricter requirements than the exchange minimum.

Some futures brokers offer reduced intraday margin during specified trading hours. These requirements may be much lower than the amount required to hold the same contract beyond the broker’s intraday cutoff.

That lower number can make a contract appear more accessible than it really is.

For example, a trader may be allowed to open a futures contract with a relatively small intraday margin requirement. If the position remains open near the broker’s cutoff, a much larger overnight or full margin requirement may apply.

If the account cannot meet it, the trader may be forced to close the position.

Reduced intraday margin does not change:

- The contract’s tick value

- The contract’s point value

- The speed at which losses can accumulate

- The market’s volatility

- The financial exposure created by the position

It only changes the capital the broker requires for access during a particular period.

A small margin requirement can therefore sit underneath a large amount of market exposure.

Buying Power Is Not a Position-Sizing Recommendation

One of the most common margin mistakes is allowing available buying power to determine position size.

A platform may show enough buying power for five contracts. That does not mean five contracts are appropriate. It only means the account currently satisfies the broker’s access requirements for that quantity.

The broker is not evaluating the quality of the setup.

It does not know whether the entry is in the middle of a range, whether the stop is structurally valid, or whether the trader is reacting emotionally. It does not know whether the trader has already taken several losses that day.

It is performing an account calculation.

Suppose a trader has enough buying power to open ten micro futures contracts. If each contract is worth $5 per point, the combined position changes by:

10 contracts × $5 per point = $50 per point

A ten-point adverse move would represent:

10 points × $50 per point = $500

The word micro does not make that combined position small. Contract quantity has rebuilt the exposure of a larger contract.

The mistake feels reasonable because buying power appears as permission. The order ticket is available, the account meets the requirement, and the platform will accept the trade.

But technical permission is not risk approval.

The cleaner question is:

How many contracts fit the planned stop and acceptable dollar risk?

That calculation should determine quantity—not the maximum number the broker allows.

Margin and Trade Risk Must Be Calculated Separately

Margin and planned risk belong in the same trade evaluation, but they perform different jobs.

Margin determines whether the position can be opened and maintained. Planned risk determines whether the financial consequence of being wrong is acceptable.

Suppose a trader is considering a futures position with:

- A four-point distance from entry to invalidation

- A contract value of $5 per point

- Three contracts

The planned price risk is:

4 points × $5 × 3 contracts = $60

That $60 is the calculated price risk if the stop fills at the intended level. Commissions, fees, spread, and slippage may increase the final loss. Those additional expenses are explained in the real cost of a trade.

The broker’s margin requirement might be higher or lower than $60. That does not change the stop-based calculation.

This gives the trader two separate checks:

- Margin check: Can the account support the position under the broker’s requirements?

- Risk check: Is the planned loss appropriate for the account and setup?

A trade should pass both.

Passing the margin check alone is not enough.

Margin Does Not Cap the Loss

Another dangerous misunderstanding is treating the margin deposit as the maximum amount that can be lost.

Margin is not a prepaid loss limit.

A leveraged position can lose more than the margin originally required to open it. In severe conditions, losses may also exceed the capital currently sitting in the account, depending on the product, market movement, liquidity, and account agreement.

A stop order can help manage risk, but it cannot guarantee an exact exit price. A sudden gap, rapid move, thin order book, or trading interruption can cause the final fill to occur beyond the requested stop level.

That is why position size matters even when a stop is used.

A trader who sizes the position only because the account meets the margin requirement may leave too little room for normal movement, execution uncertainty, or an unexpected market event.

The correct sequence is not:

- See how many contracts the broker permits

- Open the maximum quantity

- Find a stop that makes the loss acceptable

The cleaner sequence is:

- Identify the setup and invalidation level

- Measure the distance from entry to invalidation

- Convert that distance into dollars per contract

- Choose a quantity that fits the account’s risk limit

- Confirm that the account also satisfies the margin requirement

The market structure should define the stop. The acceptable dollar risk should define the quantity.

Margin is a final access check, not the starting point for trade construction.

Available Margin Can Shrink Quickly

Available margin is the remaining account capacity after open positions and current account equity are considered.

It can change as the market moves.

When an open position loses value, account equity may fall. At the same time, the account’s remaining ability to support other positions may decrease. A trader who uses nearly all available margin can therefore lose flexibility at the exact moment it is needed most.

The account may have little capacity to absorb:

- Normal adverse movement

- Higher margin requirements

- Additional volatility

- Slippage

- Multiple correlated positions moving together

- An overnight requirement

- A broker risk adjustment

Using less than the maximum available buying power is not wasted capacity. It creates room for uncertainty.

That room protects decision quality.

A trader with excess capacity can evaluate the next decision more calmly. A trader operating near the margin limit may be forced to react to account mechanics instead of market structure.

A Better Margin Checklist

Before entering a leveraged position, a trader should know:

- The contract’s notional or total market exposure

- The tick size and tick value

- The dollar value of one point

- The current initial margin requirement

- The current maintenance margin requirement

- Whether intraday and overnight requirements differ

- The broker’s liquidation policy

- The planned stop distance

- The dollar risk per contract

- The total dollar risk for the full position

- The remaining account capacity after entry

These values should be verified through the broker, exchange, and trading platform. Margin requirements and policies can change.

A useful final question is:

Am I choosing this position because the trade structure supports it, or because the broker gives me enough buying power to open it?

That question separates risk management from access.

For broader instruction on entries, exposure, stops, and trade construction, continue through The Basics curriculum. The next concept is what leverage is and why it cuts both ways.

Traders building their foundation from the beginning can also start with the beginner trading path.

Final Thought

Margin is the deposit behind leveraged exposure. It allows a trader to control a position without paying its full value upfront.

That convenience can make a large position look smaller than it is.

Initial margin determines what is required to open the position. Maintenance margin helps determine whether it can remain open. Neither number tells the trader where the setup becomes invalid or how much should be risked.

Buying power is not a recommendation.

The better process is to define the trade, calculate the stop-based dollar risk, choose the appropriate position size, and then confirm that the account satisfies the margin requirement.

Margin determines access.

Risk management determines whether that access should be used.

Educational content only. Trading involves substantial risk and is not suitable for everyone.